Effects of COVID-19 on accounting professionals’ job behaviors, focusing on the moderating effect of organizational communication

Abstract

BACKGROUND:

The coronavirus disease (COVID-19) caused mandatory lockdowns across all organizations. Telework generated challenges in workflow due to limited organizational communication.

OBJECTIVE:

This study seeks to examine the impact of pre-, during, and post-COVID-19 on accounting professionals’ job behaviors and tests the moderating effect of organizational communication. Also, the study aims to provide implications for practitioners from the findings.

METHODS:

Survey data for accounting professionals working in North Carolina across COVID-19 time periods was collected to achieve a sample size of 333. Pairwise t-tests and hierarchical regression analyses were applied to test the hypotheses.

RESULTS:

The results suggest a statistically significant difference across certain time periods for job performance and turnover intentions but not job satisfaction. Furthermore, organizational communication moderates the relationship between post-COVID-19 and job performance and turnover intentions but not job satisfaction.

CONCLUSIONS:

Organizations should search for ways to enhance organizational communication to increase employee perceived job performance and decrease employee turnover intentions.

Dr. Dena Breece is an Assistant Professor of Accounting at the Thomas College of Business and Economics, University of North Carolina at Pembroke. She received her Ph.D. in Business Administration with a concentration in accounting and finance from Trident University International in Cypress, CA. Dr. Breece has served over 17 years in academics, over 20 years in the accounting industry, and is a Certified Public Accountant. Her research interests are managerial accounting, technology, and pedagogy. She has published articles in the Journal of Accountancy, the Journal of Case Research and Inquiry, the Southeast Case Research Journal, and various conference proceedings.

Dr. SiAhn Mehng is an Associate Professor of Management at the Thomas College of Business and Economics, University of North Carolina at Pembroke. She received her Ph.D. in Business Administration at the Carlson School of Management, University of Minnesota-Twin Cities. Her research interests are diversity management, gender, stereotypes, and prosocial/counterproductive behaviors. Dr. Mehng’s work has appeared in the Academy of Management Journal. She also presented a number of her articles at the Academy of Management Annual Meeting and the Society for Industrial and Organizational Psychology Annual Conference.

Dr. Daniel Parisian is an Assistant Professor of Economics in the Thomas College of Business and Economics at the University of North Carolina at Pembroke. Dr. Parisian received his Ph.D. in Economics from Binghamton University, State University of New York. He is an applied microeconomist whose primary research interests lie in the evaluation of active labor market programs, education, health, and craft breweries. Dr. Parisian has recently published in Applied Economics, Economics of Education Review, and Research in Labor Economics, as well as presented at international, national, and regional conferences.

Dr. Stephen Moore is a faculty member at the Belk College of Business, University of North Carolina at Charlotte. He earned an MBA and Ph.D. from Syracuse University. He has been active in educational settings for over 30 years. Dr. Moore presented at the Lilly Conference on Teaching and Learning, the United States Association for Small Business and Entrepreneurship, and other conferences. He has owned several businesses including a consulting and education firm. His business ownership experience enables him to bring real-world experience to his students. Dr. Moore taught business and entrepreneurship courses in the US, China, and South Korea.

1Introduction

The coronavirus disease (COVID-19) caused numerous challenges to all types of organizations across all nations [1], and many countries implemented lockdown restrictions to prevent and slow down the spread of the virus [2, 3]. Accounting professionals also could not avoid the impact on their work environment. With lockdown restrictions, accounting organizations were forced to change their policies and procedures to enable remote work settings, and this new practice brought many challenges. A survey conducted by the Association of International Certified Professional Accountants (AICPA) showed that hiring and maintaining staff ranked high as the most important concern among all Certified Public Accountant (CPA) firms, and managing a hybrid workforce (i.e., remote and in-person) was a big concern among mid-to-large size CPA firms [4].

With this major shift, accounting organizations had to pivot as well in order to manage hybrid working environments while protecting their employees. A survey collected from more than 1,000 U.S. accounting firms by the 2021 National Management of an Accounting Practice showed that a median of 50% of top-performing CPA firms have their employees working remotely, and as a whole, a median of 30% of CPA firms have remote employees [5]. With more requests from employees, accounting firms had to embrace a remote or hybrid model, but accounting firm leaders shared several challenges, including establishing formal and fair policies, monitoring productivity, ensuring everyone’s visibility, and limited learning opportunities [6, 7]. To face related challenges, firms put more effort into building up career planning, hosting entertaining activities, and installing more technology to monitor performance and communication [6, 7].

Clear, simplified, and open organizational communication has been emphasized in some accounting firm leaders’ interviews [6, 7]. However, minimal research has been conducted on organizational communication as it relates to the pandemic and accounting professionals’ job behaviors. Some researchers have suggested the significant role of information and communication technology in education during the pandemic [8] and environmental sustainability [9, 10]. However, with differences in industry and context, these findings may not extend to accounting professionals. A few studies on organizational communications during the pandemic show the direct influence on certain job behaviors [11, 12], but a deeper discussion and conceptualization of organizational communication is missing.

The goal of the current study is to fill this gap in the literature by testing the moderating effect of organizational communication on employees’ job behaviors focusing on accounting professionals over the pre-, during, and post-COVID-19 time periods. First, we review the effect of COVID-19 on employee work behaviors within the communication channel and information richness theory [13]. Then, we theorize the positive effect of active interpersonal communication from supervisors in the pandemic context. Second, we collected survey data from accounting professionals with a final sample size of 333 to test our hypotheses. Third, we discuss the study findings and implications for practitioners.

Our research contributes to the management literature in several ways. First, we collected data from accounting professionals to examine their job behaviors and performance in the pandemic and crisis context. Second, we highlight the importance of organizational communication on employee job behaviors and performance, specifically, how organizational communication can positively increase employee job behaviors and performance in the post-pandemic period. Lastly, our research provides practical insights for organizations regarding how employee behaviors and performance can continue to improve post-pandemic.

2Literature review and hypotheses

2.1The effect of COVID-19 on employee job behaviors

The COVID-19 pandemic forced organizations to switch the operation process to meet lockdown restrictions. This sudden change demanded a shift to teleworking for office employees, which had a significant influence on employee job behaviors. After millions of employees were sent to work from home in March 2020, a “Great Resignation” occurred as 47.8 million Americans quit their jobs in 2021, and 50.5 million quit in 2022 [14, 15]. Pandemic remote work was the catalyst for the “Great Resignation” when individuals sought better pay or work-life balance [16]. LinkedIn data showed that one in six posted jobs had a remote or hybrid work component at the end of 2021, compared to one in 67 in March 2020 [17]. Meanwhile, a quarter of employees who resigned and changed their jobs expressed regret about leaving their previous job, leading to the “Great Regret” [18]. With inflation and rising interest rates, premature retirees returned to the workforce, and individuals who couldn’t fit into the new role or new management culture decided to return to their previous workplace [18]. Therefore, as an alternative to resigning, employees began “Quiet Quitting” by “opting out of tasks beyond one’s assigned duties and becoming less psychologically invested in work” [19]. These new job behavior trends suggest positive work attitudes seemed harder to maintain during the pandemic.

Management literature shows mixed findings that the pandemic had negative effects on employee job behaviors, but some contingent factors negate the effect. First, Newman and colleagues [20] reviewed organizational behavior articles published over the first two years of the pandemic. Regarding employee work attitudes, several researchers focused on attitudes related to remote working, and the overall findings show that working from home negatively impacted work-life balance, decreased job satisfaction, and increased turnover intentions [21]. Regarding employee performance, key findings still support the previously established predictors that employees who were more satisfied, engaged, and committed to their jobs also performed better during the pandemic [22]. Similarly, a few studies showed negative work attitudes impacted by stress and emotions (e.g., anxiety [23]). Ployhart and colleagues [24] compared the pre-pandemic and pandemic periods and found that COVID-19 was negatively related to the work engagement of new hires. Bajrami and colleagues [25] examined the impact of COVID-19 on employees’ work attitudes through job insecurity. The results show that job insecurity, risk-taking behavior, and fairness of organizational changes were negatively related to both job satisfaction and turnover intentions. Changes in the business and the possibility of business closure caused employees to be less satisfied but less willing to leave their jobs. Syrek and colleagues [26] examined pandemic-related changes in workload, autonomy, work-nonwork balance, work engagement, and job satisfaction. The results show that job satisfaction increased during the pandemic when employees perceived organizational support, but job satisfaction decreased when governmental prevention measures were relaxed, and workers returned to the office instead of working from home.

Taken together, we test whether employee job behaviors, specifically job satisfaction, job performance, and employee turnover intentions, changed across the periods of pre-, during, and post-COVID-19.

H1: Employee job satisfaction, job performance, and turnover intention show different tendencies pre-, during, and post-COVID-19 periods.

2.2Organizational communication

Communication is defined as “a process by which information and meaning is transferred from a sender to a receiver [27 p325].” Communication effectiveness is a crucial factor of overall organizational success, and organizational communication includes more complicated information processing (i.e., uncertainty and equivocality) than individual communication [13]. Organizational structure allocates tasks to individuals and groups where the systems’ design ensures effective communication and collaboration. Organizational communication plays a crucial role in enabling interactions and information exchange, which are essential for coordinating and managing the activities of the organization [13].

Before COVID-19, telework was considered an exceptional work arrangement due to managers’ mistrust that some employees might not put in the necessary effort when not physically supervised [28, 29]. However, the pandemic and lockdowns compelled organizations to re-learn some skills for effective planning, leadership, and coordination in a virtual workplace [30]. With mandated telework, organizations heavily relied on web-conferencing tools; however, learning how to collaborate in a virtual setting was extra challenging, especially when all communication occurred online [13].

The choice of communication channel can either improve or distort the intended message because every communication channel, whether it is written, electronic, or in-person, has unique characteristics that make it appropriate for specific circumstances while less effective in others [31]. Daft [27] explains that channel richness refers to the amount of information that can be conveyed during a communication interaction and that the available communication channels can be classified into a hierarchy based on information richness. The richness of an information channel is influenced by three characteristics: (1) the ability to handle multiple cues simultaneously, (2) the ability to facilitate rapid, two-way feedback, and (3) the ability to establish a personal focus for communication [27 p341–342]. Based on the three characteristics, Daft [27] suggests that face-to-face discussions are the richest medium, allowing direct interaction with multiple information cues. Video conference tools are next because they still allow some eye contact and immediate feedback. Telephone conversations, digital written messaging, and memos or letters follow in the richness continuum as those lack either visual or verbal information cues [27 p342–343].

As face-to-face discussions have the richest information, forced telework settings could be challenging for both managers and employees [32]. A study analyzing digital communication patterns during the pandemic suggested that employees’ day-to-day work activities have changed to spending less time in meetings per day (–11.5 percent) with more email communications, but significant increases in the length of the average workday (+48.5 minutes) [33]. A similar tendency was also found in a study [29] that the workday significantly increased at the beginning of all virtual work, and that the average workdays were still 10% to 20% longer even when the trends moved back towards pre-COVID-19 work environments. These findings reflect the organizations’ struggle to maintain smooth operations during the pandemic crisis with different communication patterns.

As organizations shift towards virtual environments, organizations encounter challenges linked to eliminating a physical office and the continued absence of in-person interpersonal engagement [34]. Managers needed to reacquire certain soft skills to maintain operations. For instance, when the COVID-19 pandemic disrupted the organization’s production processes and services, managers had to identify effective methods to engage with employees and show their support. A couple of studies during the pandemic showed the positive impact of this effort that employee engagement and knowledge sharing were positively related to organizational performance [35] and organizational support was positively related to job satisfaction and organizational commitment [36]. It is beneficial for employees, especially during crises, that their leaders are actively developing communication strategies (e.g., [37]) so employees have a clear idea of their tasks, performance, and development.

After a sudden lockdown and shift to a remote work setting, employees faced challenges in accessing and utilizing information to keep operations running. In unstable work environments, employees encounter challenges related to trust, motivation to share information, technical competencies, and degrees of organizational commitment, which potentially lead to personal disconnection [38]. When organizations heavily depend on virtual communication, managers should recognize the significance of interpersonal relationships within their work unit [39]. Therefore, in this study, we conceptualize effective organizational communication as interpersonal communication between managers and subordinates that encompasses both task efficiency and the personal development of employees.

Indeed, some research shows the effectiveness of organizational communication on employee job behaviors during the COVID-19 pandemic. For example, Almohtaseb and colleagues [11] reviewed several studies that show a positive relationship between effective communication, job satisfaction, and job performance. They also found a strong positive relationship between effective communication and job satisfaction during COVID-19. Also, Yue and colleagues [12] found that when supervisors used empathetic communication during organizational change, employees perceived a higher level of affective trust in their supervisors. This, in turn, led to more positive relationships between employees and the organization. As a result, these positive employee-organizational relationships had a negative relationship with employee turnover intention.

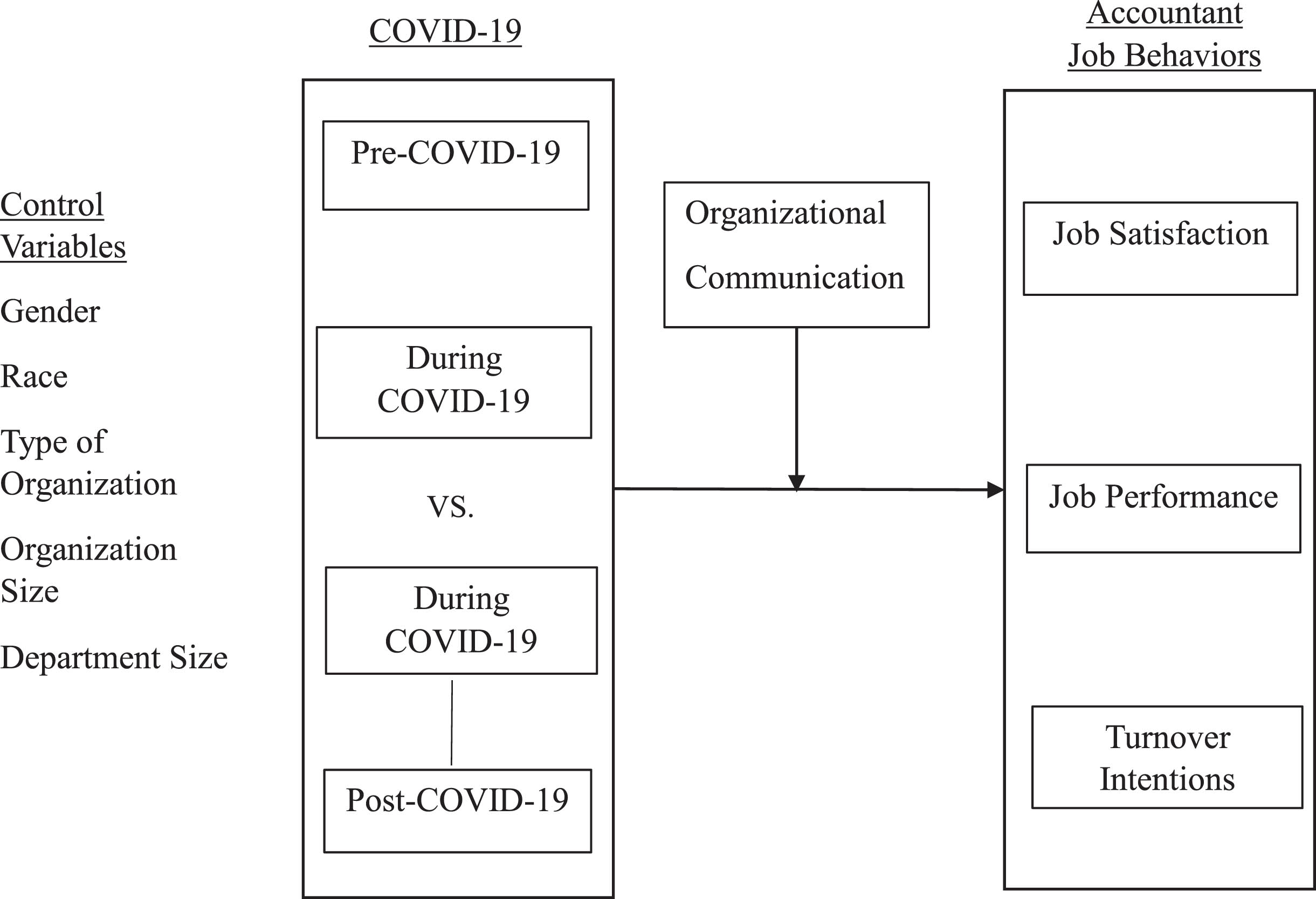

We propose that accounting professionals also encountered sudden changes in operational procedures due to COVID-19 lockdowns and subsequent easing of restrictions. During the change process, all employees would have required a new understanding of organizational goals, the scope of employee work, and the foundational procedures necessary to achieve both employee and organizational goals. In the virtual communication process, we assume that some employees may have felt left out of the decision-making and problem-solving loop, possibly causing low morale. As organizations and employees transition from pre-COVID-19 to the “new normal” during COVID-19, and eventually to post-COVID-19, we posit that organizational communication influences the job behaviors of accounting professionals. In this study, depicted in Fig. 1, we investigate the moderating effects of organizational communication on the relationships between different periods surrounding COVID-19 and employee job behaviors. Specifically, our hypotheses test how the intensity of organizational communication moderates the relationship between the pre-COVID-19, during COVID-19, and post-COVID-19 periods with the employee job behaviors such as job satisfaction, job performance, and turnover intentions.

Fig. 1

Theoretical framework.

H2: Organizational communication moderates the relationship between COVID-19 periods and job satisfaction, so as organizational communication increases, job satisfaction increases.

H3: Organizational communication moderates the relationship between COVID-19 periods and job performance, so as organizational communication increases, job performance increases.

H4: Organizational communication moderates the relationship between COVID-19 periods and turnover intention, so as organizational communication increases, turnover intention decreases.

3Data and methodology

3.1Sample and procedure

We collected survey data from accounting professionals working within the same organization in North Carolina in the United States pre-, during, and post-COVID-19. Our survey was distributed through professional accounting organizations like the North Carolina Association of Certified Public Accountants, the Institute of Management Accountants, the Association of Certified Fraud Examiners, the North Carolina Governmental Finance Officers Association, and the Association of International Certified Professional Accountants. An invitation to participate in our study was communicated to members through the professional organization’s online community forum or listserv. Participants were encouraged to share the invitation with accounting professionals within their organization. Participation in the study was voluntary, with responses kept confidential.

Usable surveys were identified as responses from subjects working in accounting positions in public accounting firms, business and industry or “industry” (public and private companies), governmental agencies, or other organizations in North Carolina pre-, during, and post-COVID-19. The initial sample consisted of 594 respondents. The data was analyzed to remove incomplete survey responses and data from respondents working outside North Carolina. Our final balanced sample contained 111 usable surveys. In examining cross-sectional data across the three periods, the panel dataset contained 333 observations.

Table 1 shows the final sample contained more female respondents (71.17%) than male respondents (28.83%). Furthermore, most of the participants were Caucasian (86.49%). Concerning the organization, the final sample consisted of individuals working primarily in public accounting firms (55.86%) compared to other organizations (industry 18.92%, governmental agencies 18.02%, and other organizations 7.21%). The organization size ranged from 1 to 10 employees (23.42%) to 126 and over employees (37.84%). Finally, the accounting department size was small (1–10 employees at 40.54%) as compared with medium (11–21 employees at 25.23%) or large (22 or more employees at 34.23%) departments.

Table 1

Descriptive characteristics of respondents (n= 111)

| Demographic | Description | Number of | Percent |

| characteristics | respondents | ||

| Gender | Male | 32 | 28.83 |

| Female | 79 | 71.17 | |

| Race | African American | 5 | 4.50 |

| American Indian or Alaska Native | 4 | 3.60 | |

| Asian or Asian American | 3 | 2.70 | |

| Caucasian | 96 | 86.49 | |

| Multi-ethnic | 2 | 1.80 | |

| Native Hawaiian or other Pacific Islander | 1 | 0.90 | |

| Type of Organization | Public Accounting Firm | 62 | 55.86 |

| Industry | 21 | 18.92 | |

| Government | 20 | 18.02 | |

| Other | 8 | 7.21 | |

| Organization Size | 1–10 employees | 26 | 23.42 |

| 11–25 employees | 16 | 14.41 | |

| 26–50 employees | 13 | 11.71 | |

| 51–75 employees | 6 | 5.41 | |

| 76–125 employees | 8 | 7.21 | |

| 126 and over employees | 42 | 37.84 | |

| Department Size | Small 1–10 employees | 45 | 40.54 |

| Medium 11–21 employees | 28 | 25.23 | |

| Large 22 or more employees | 38 | 34.23 |

3.2Study measures

We used restriction dates imposed on North Carolina organizations to establish timeframes. Restrictions on in-person work were placed into effect on March 30, 2020 [40]. Therefore, for the purposes of this study, we measured pre-COVID-19 as on or before March 29, 2020. Furthermore, we defined the during COVID-19 period as March 30, 2020 through April 30, 2021, to be consistent with the restrictions. May 2021 was considered a transition month as restrictions were being phased out. As of June 1, 2021, North Carolina restrictions were lifted [41]. We measured the post-COVID-19 period as June 1, 2021, and after. Survey respondents were asked the same questions related to organization communication and job behaviors over all three periods, and we created dummy variables to distinguish each period for the empirical analysis.

The levels of variables were measured on Likert scales as adapted from prior instruments. We adapted Spector [42] to develop a measure of job satisfaction based on the communication satisfaction items relevant to our study. Survey item examples included “Communications seem good within this organization.” and “Work assignments are often not fully explained.” [42 p75–76]. Additionally, we asked respondents, “Are you satisfied with your job?” Responses were measured on a 6-point Likert scale ranging from “1 = disagree very much” to “6 = agree very much.” We utilized Yousef [43] to measure job performance. Respondents were instructed to respond with their perceptions regarding job performance and not actual performance evaluations received. The survey item example includes ”How do you evaluate the performance of yourself at your job compared with your peers doing the same kind of work?” [43 p13]. Responses were measured on a 7-point Likert scale ranging from “1 = very low” to “7 = very high.” We further adapted Vermeir et al.’s [44] use of a prior survey by van Veldhoven and Meijman [45] to measure turnover intentions. The survey item example includes, “Sometimes, I think about changing jobs.” [44 p24]. Responses were measured on a 6-point Likert scale ranging from “1 = disagree very much” to “6 = agree very much.” We adapted the survey by Penley and Hawkins [46], which included five categories of supervisor communication often held with subordinates. Concerning task communication, we asked, “My supervisor lets us know about changes coming up.” [46, p. 313]. Concerning performance communication, we asked, “My supervisor lets me know which areas of my performance are weak.” [46, p. 313]. Concerning career communication, we asked, “My supervisor discusses with me how to get additional training.” [46, p. 314]. Concerning communication responsiveness, we asked, “When I ask a question, my supervisor does his/her”/their “best to get me a response.” [46, p. 314]. Finally, concerning personal communication, we asked, “My supervisor asks about my interests outside of work.” [46, p. 314]. Responses were measured on a 6-point Likert scale ranging from “1 = disagree very much” to “6 = agree very much.”

The empirical analyses were based on initial tests of our dependent variables and moderator between the COVID-19 periods, as well as the validity of their construction. With our survey questions for each measure, we tested the consistency and reliability of the responses using Cronbach’s alpha, which are presented in Table 2. All but one of our constructs, job satisfaction during COVID-19, are acceptable at values greater than 0.7, though the pre- and post-COVID-19 job satisfaction measures are only slightly greater than 0.7. The other constructs, job performance, turnover intentions, and organizational communication, all have Cronbach’s alpha measures greater than 0.8, proving their reliability [47].

Table 2

Cronbach’s alpha results

| Constructs | Items | Pre-COVID-19 | During-COVID-19 | Post-COVID-19 |

| Job Satisfaction | 5 | 0.7237 | 0.6720 | 0.7045 |

| Job Performance | 4 | 0.8410 | 0.8207 | 0.8314 |

| Turnover Intentions | 4 | 0.8998 | 0.9029 | 0.8948 |

| Organizational Communication | 5 | 0.8281 | 0.8203 | 0.8081 |

| n | 111 | 111 | 111 |

Control variables at the employee and organization levels were considered. Employee level controls were gender and race. Organization level controls were the type of organization, organization size, and accounting department size.

Table 3 shows summary statistics of the variables from survey data across pre-, during, and post-COVID-19 time periods. First, job satisfaction was the highest pre-COVID-19, with a minimal decrease during COVID-19 that remained consistent post-COVID-19. Second, job performance was strongest pre-COVID-19, decreased during COVID-19, and slightly increased post-COVID-19. Third, turnover intentions were largest post-COVID-19 compared to the during COVID-19 and pre-COVID-19 periods. Finally, organizational communication increased post-COVID-19 after having declined during COVID-19 compared to pre-COVID-19.

Table 3

Summary statistics of variables (n= 111)

| Variable | Item | Mean | Standard Deviation |

| Job Satisfaction | Pre-COVID-19 | 3.2901 | 0.5744 |

| During COVID-19 | 3.2757 | 0.5933 | |

| Post-COVID-19 | 3.2775 | 0.6221 | |

| Job Performance | Pre-COVID-19 | 5.4459 | 1.1101 |

| During COVID-19 | 5.2590 | 1.0676 | |

| Post-COVID-19 | 5.4122 | 1.0094 | |

| Turnover Intentions | Pre-COVID-19 | 2.3491 | 1.3961 |

| During COVID-19 | 2.2703 | 1.3366 | |

| Post-COVID-19 | 2.4842 | 1.4127 | |

| Organizational Communication | Pre-COVID-19 | 4.5027 | 1.1102 |

| During COVID-19 | 4.4613 | 1.1184 | |

| Post-COVID-19 | 4.6378 | 1.0725 |

3.3Empirical model

This study examines whether organizational communication intensifies the influence of COVID-19 related periods on various employee behaviors amongst accounting professionals in the state of North Carolina. Specifically, we test if organizational communication acts as a moderator across the pre-, during, and post-COVID-19 periods with regard to employee self-reported job satisfaction, job performance, and turnover intentions using regression analysis. Through a hierarchical model approach, we estimate three separate regression models across our three dependent variables, job satisfaction, job performance, and turnover intentions. The three regression models are described below.

In the first step, we run regressions on our dependent variables over the set of control variables described in section 3.2. These controls may relate to employee behaviors but are not the focus of this study.

In the second step, we include our independent variables to the control variables from the first step regressions. The first group of independent variables are the indicator/dummy variables for the pre-, during, and post-COVID-19 periods. For the regression analysis, our reference group is the during COVID-19 period. Therefore, regression coefficients on the pre- and post-COVID-19 variables will be interpreted with respect to the during COVID-19 period. The last independent variable is a measure of organizational communication.

In the third step, we include our moderator to the second step regressions. Following the methods described by Helm and Mark [48], the moderator effect is identified by the coefficients on the interaction terms between the dummy variable for each period and organizational communication. Again, the reference period is during COVID-19, and any statistically significant coefficients on the interaction terms are interpreted against this period. Following our hypotheses and review of the literature, we expect the sign of the moderator coefficients to be positive with respect to job satisfaction [11, 36] and job performance [11, 49] but negative for turnover intentions [12].

4Data analysis and results

Before estimating our hierarchical regression, we perform t-tests of the dependent variable means across all pairwise COVID periods to see if there is suggestive evidence of differences across the various periods. These pairwise t-tests are used to test hypothesis H1, and the results are presented in Table 4. H1 states that employee job satisfaction, job performance, and turnover intentions vary across the pre-, during, and post-COVID-19 periods. The t-tests show that there are only statistically significant differences with regards to job performance between the pre-during and during-post COVID-19 periods, at a significance level of p < 0.05. There is a marginally significant difference in means for turnover intentions between the during-post COVID-19 period, at a level of p < 0.10. To summarize, the paired t-tests provided support for three of the nine pairwise time periods hypothesized in H1.

Table 4

Employee behaviors independent sample t-tests for equality of means

| Employee | COVID | T | df | Sig. | Mean | Std. error | 95% Confidence interval | |

| behavior | periods | (2-tailed) | difference | difference | of the difference | |||

| Lower | Upper | |||||||

| Job Satisfaction | Pre vs. During | 0.2977 | 110 | 0.7665 | 0.0144 | 0.0484 | –0.0815 | 0.1104 |

| During vs. Post | –0.0647 | 110 | 0.9485 | –0.0018 | 0.0279 | –0.0570 | 0.0534 | |

| Pre vs. Post | 0.2327 | 110 | 0.8164 | 0.0126 | 0.0542 | –0.0948 | 0.1200 | |

| Job Performance | Pre vs. During | 2.8459 | 110 | 0.0053 | 0.1869 | 0.0657 | 0.0568 | 0.3171 |

| During vs. Post | –2.3296 | 110 | 0.0217 | –0.1532 | 0.0657 | –0.2834 | –0.0229 | |

| Pre vs. Post | 0.4327 | 110 | 0.6661 | 0.0338 | 0.0781 | –0.1210 | 0.1885 | |

| Turnover Intentions | Pre vs. During | 0.8743 | 110 | 0.3839 | 0.0788 | 0.0902 | –0.0998 | 0.2575 |

| During vs. Post | –1.9131 | 110 | 0.0583 | –0.2140 | 0.1118 | –0.4356 | 0.0077 | |

| Pre vs. Post | –1.2255 | 110 | 0.2230 | –0.1351 | 0.1103 | –0.3537 | 0.0834 | |

The results from the hierarchical regression models are presented in Table 5. Sections 4.1–4.3 discuss the results from the regression analyses based on the various outcome measures and their implications for hypotheses H2-H4.

Table 5

Hierarchical regression results

| Job Satisfaction | Job Performance | Turnover Intentions | |||||||

| Variables | bstep1 | bstep2 | bstep3 | bstep1 | bstep2 | bstep3 | bstep1 | bstep2 | bstep3 |

| Constant | 3.337 (0.211)** | 3.518 (0.260)** | 3.497(0.316)** | 6.309 (0.345)** | 4.573 (0.391)** | 5.078 (0.472)** | 2.200 (0.449)** | 4.180 (0.511)** | 3.495 (0.617) ** |

| Government Org. | 0.287 (0.146)* | 0.270 (0.147) | 0.272 (0.147) | –0.860 (0.238)** | –0.716 (0.220)** | –0.738 (0.220)** | –0.089 (0.310) | –0.275 (0.288) | –0.248 (0.288) |

| Industry Org. | –0.131 (0.145) | –0.130 (0.146) | –0.130 (0.146) | –0.258 (0.238) | –0.261 (0.219) | –0.270 (0.218) | –0.092 (0.309) | –0.089 (0.286) | –0.078 (0.285) |

| Public Accountant Org. | 0.057 (0.141) | 0.080 (0.142) | 0.081 (0.143) | –0.517 (0.231) * | –0.720 (0.214)** | –0.725 (0.214)** | –0.042 (0.300) | 0.217 (0.280) | 0.221 (0.279) |

| 1–10 Employees in Org. | –0.029 (0.173) | –0.070 (0.176) | –0.068 (0.177) | –0.417 (0.282) | –0.066 (0.265) | –0.093 (0.264) | 0.566 (0.367) | 0.117 (0.345) | 0.151 (0.345) |

| 11–25 Employees in Org. | –0.305 (0.163) | –0.341 (0.166)* | –0.340 (0.167)* | –0.159 (0.267) | 0.155 (0.250) | 0.137 (0.249) | –0.007 (0.347) | –0.410 (0.326) | –0.386 (0.325) |

| 26–50 Employees in Org. | –0.115 (0.167) | –0.153 (0.170) | –0.152 (0.170) | –0.427 (0.273) | –0.101 (0.255) | –0.113 (0.254) | 0.152 (0.355) | –0.265 (0.333) | –0.250 (0.332) |

| 76–125 Employees in Org. | –0.050 (0.178) | –0.060 (0.179) | –0.060 (0.179) | –0.246 (0.291) | –0.155 (0.269) | –0.168 (0.268) | –0.486 (0.378) | –0.602 (0.351) | –0.587 (0.350) |

| 126 + Employees in Org. | 0.013 (0.154) | 0.015 (0.155) | 0.016 (0.155) | –0.596 (0.252)* | –0.621 (0.232)** | –0.633 (0.232)** | 0.359 (0.328) | 0.391 (0.304) | 0.406 (0.303) |

| Small Accounting Dept. | –0.172 (0.108) | –0.136 (0.112) | –0.137 (0.112) | 0.417 (0.176)* | 0.104 (0.168) | 0.118 (0.167) | –0.935 (0.229)** | –0.534 (0.219)* | –0.553 (0.218)* |

| Large Accounting Dept. | –0.020 (0.096) | –0.028 (0.097) | –0.029 (0.097) | 0.241 (0.157) | 0.319 (0.145) | 0.323 (0.145)* | –0.713 (0.205)** | –0.812 (0.190)** | –0.818 (0.189)** |

| Female | 0.027 (0.075) | 0.022 (0.076) | 0.022 (0.076) | –0.099 (0.123) | –0.058 (0.114) | –0.062 (0.113) | 0.360 (0.160)* | 0.307 (0.149)* | 0.313 (0.148)* |

| American Indian/Alaskan Native | –0.090 (0.185) | –0.109 (0.186) | –0.107 (0.188) | 0.392 (0.303) | 0.560 (0.280)* | 0.518 (0.280) | 0.751 (0.394) | 0.536 (0.366) | 0.587 (0.366) |

| Asian | –0.004 (0.203) | –0.009 (0.203) | –0.010 (0.205) | –0.827 (0.332)* | –0.784 (0.306)* | –0.777 (0.306)* | 1.637 (0.431)** | 1.582 (0.399)** | 1.577 (0.399)** |

| Black/African American | –0.325 (0.160)* | –0.327 (0.160)* | –0.328 (0.161)* | –0.531 (0.261)* | –0.514 (0.241)* | –0.502 (0.240)* | 0.525 (0.340) | 0.306 (0.702) | 0.489 (0.314) |

| Hispanic | 0.325 (0.108)** | 0.322 (0.109) ** | 0.322 (0.109)** | –1.104 (0.177)** | –1.077 (0.163)** | –1.079 (0.163)** | 1.586 (0.230)** | 1.552 (0.213)** | 1.553 (0.213)** |

| Native Hawaiian/Pacific Islander | –0.852 (0.356)* | –0.875 (0.357)* | –0.877 (0.359)* | –2.873 (0.582)** | –2.673 (0.537)** | –2.630 (0.536)** | 0.563 (0.757) | 0.306 (0.702) | 0.251 (0.700) |

| Multi–Race | –0.683 (0.234)** | –0.621 (0.239)** | –0.621 (0.240)** | –0.224 (0.382) | –0.763 (0.360)* | –0.759 (0.359)* | 1.510 (0.497)** | 2.201 (0.470)** | 2.194 (0.468)** |

| Independent Variables | |||||||||

| Pre–COVID-19 | 0.016 (0.075) | 0.028 (0.314) | 0.172 (0.113) | –0.358 (0.469) | 0.098 (0.147) | 0.877 (0.612) | |||

| Post–COVID-19 | 0.009 (0.075) | 0.056 (0.325) | 0.089 (0.113) | –0.867 (0.486) | 0.296 (0.148)* | 1.537 (0.635)* | |||

| Org. Comm. | –0.042 (0.032) | –0.037 (0.051) | 0.362 (0.049)** | 0.253 (0.076)** | –0.463 (0.063)** | –0.315 (0.099)** | |||

| Moderator Effects | |||||||||

| Pre–COVID-19 x Org. Comm. | –0.003 (0.068) | 0.119 (0.102) | –0.174 (0.133) | ||||||

| Post–COVID-19 x Org. Comm. | –0.010 (0.070) | 0.210 (0.104)* | –0.273 (0.136)* | ||||||

| R2 | 0.169 | 0.174 | 0.174 | 0.304 | 0.414 | 0.422 | 0.303 | 0.408 | 0.416 |

| ΔR2 | 0.005 | 0.000 | 0.110 | 0.008 | 0.105 | 0.008 | |||

Notes: n = 333. Reference period is the during COVID-19 period. Coefficients are reported with standard errors in parentheses. *p < 0.05; **p < 0.01.

4.1Empirical model results: Organizational communication as a moderator between COVID-19 periods and job satisfaction

As previously stated, our paired t-tests do not show any statistically significant differences in job satisfaction across the three COVID-19 periods. However, these t-tests do not account for any factors that may be associated with job satisfaction, either positive or negative. The hierarchical regression results in Table 5 also show that there were no statistically significant correlations between the various time periods and job satisfaction. Additionally, organizational communication and organizational communication as a moderator between the time periods and job satisfaction were statistically insignificant. Thus, hypothesis H2 does not hold.

4.2Empirical model results: Organizational communication as a moderator between COVID-19 periods and job performance

The initial t-tests indicate that there are differences in employee job performance for the pre-during and during-post COVID-19 periods. In the hierarchical regression analysis, as we move from step 1 to step 2 and step 2 to step 3, we find that both organizational communication and organizational communication as a moderator between the post-COVID-19 period and job performance are both statistically significant at a p < 0.05 significance level. The results also indicate that organizational communication does not act as a positive moderator for the pre-COVID-19 period. In other words, better organizational communication only improved job performance post-COVID-19, relative to the during COVID-19 period. Thus, hypothesis H3 holds for the post-COVID-19 period. As explained by the R2, the addition of the independent variables in step 2 and moderators in step 3 continually improve the explanatory power of the model.

4.3Empirical model results: Organizational communication as a moderator between COVID-19 periods and turnover intentions

There is suggestive evidence of a marginal difference between employee turnover intentions between the during and post-COVID-19 periods through our initial pairwise t-tests. However, a simple t-test does not provide any insight into this difference. The hierarchical regression analyses show that adding the independent variables and moderators improves the explanatory power of model, with the R2 improving from 0.303 to 0.408 then to 0.416. Additionally, organizational communication has a statistically significant negative effect on employee turnover intentions, as well as acts as a moderator between the post-COVID-19 period and employee turnover intentions. Thus, hypothesis H4 holds for the post-COVID-19 period.

5Discussion

5.1Theoretical implications

The purpose of this study was to understand the effects of COVID-19 on accounting professionals’ job satisfaction, job performance, and turnover intentions. Additionally, we wanted to determine the role, if any, that organizational communication plays in these employee job behaviors across the pre-, during, and post-COVID-19 periods. Empirical support was found, at least in part, for three of the four hypotheses: H1, H3, and H4. Our findings support existing literature on the positive relationship between organizational communication and job behaviors but also highlight how organizational communication can intensify positive job behaviors in the crisis context.

The pandemic changed working conditions, created opportunities for change, and implemented experiments with flexible work arrangements [50]. These and other changes were predicted to impact employee job behaviors across the three COVID-19 periods (H1). The pairwise t-tests across the three time periods showed no statistically significant differences in employee job satisfaction. This is a departure from the literature that finds job satisfaction decreases as we move through the different COVID-19 periods [21, 26]. Although our findings do not show significant differences throughout the COVID-19 period, Bernstein’s [29] survey result shows a similar tendency. In their survey, job satisfaction fell sharply after two weeks of telework, but it recovered quickly by the end of the second month. Our study sets during COVID-19 as a year and a few months (from March 30, 2020, to April 30, 2021), so concurring with Bernstein’s survey result, job satisfaction may not show a significant change over the time period.

While no significant changes were found in job satisfaction over the periods examined, the research showed significant differences in job performance and turnover intentions. Regarding job performance, there was a decrease in performance between the pre- and during COVID-19 periods but an increase between the during and post-COVID-19 periods. These significant changes align with the idea of quiet quitting [19], where employees do only what their job description entails. There was less direct monitoring with many employees working remotely during the pandemic, allowing them to complete the bare minimum tasks while working alone. However, a return to the office allowed more opportunities to work alongside colleagues, creating a more competitive atmosphere with increased performance. Finally, our pairwise t-tests showed a marginally significant decrease in turnover intentions between the during and post-COVID-19 periods. Research has shown that employees resigned through the first part of the pandemic [16, 21], but many showed regret soon after [18]. Our findings suggest that employees who stayed at the same organization throughout COVID-19 may have had similar ideas. Initially, employees may have wanted to be a part of the Great Resignation [14, 15], but they later realized that staying at their current organization was better.

The hierarchical regression results showed that organizational communication acts as a moderator for the post-COVID-19 period on some employee job behaviors. This supports the findings of Brown and Leite [51] that increases in interpersonal communication may help with positive job behaviors. First, organizational communication is positively correlated with job performance (H3), both independently (b = 0.253, p < 0.01) and as a moderator for the post-COVID-19 period (b = 0.210, p < 0.05). In other words, as organizational communication increases, so does job performance [11, 49]. Second, organizational communication is negatively correlated with turnover intentions (H4), both independently (b=–0.315, p < 0.01) and as a moderator for the post-COVID-19 period (b=–0.273, p < 0.05). This result also supports the findings of Yue et al.’s [12] study that employees prefer to stay with an organization with better communication.

A similar result to the pairwise t-tests, organizational communication did not correlate with job satisfaction nor act as a moderator for any COVID-19 period (H2). This differs from previous research that showed effective communication has a strong positive relationship with job satisfaction during COVID-19 [11]; however, this study did not compare across the COVID-19 periods.

Our findings relate to prior academic research. Similar tendencies of employee job satisfaction across pandemic timeframes were found with Berstein [29] but not in like studies [21, 26]. Regarding job performance, our results parallel the idea of quiet quitting [19] such that employees performed as required during COVID-19 periods. Thereafter, a return to their competitive work environment post-COVID-19 resulted in employees increasing their job performance. Employee turnover intentions decreased during to post-COVID-19 likely due to employees’ belief that returning to their own organization was preferred as opposed to being a part of the Great Resignation [14, 15]. Finally, our findings align with prior academic research that increased interpersonal communication results in increased positive job behaviors like job performance consistent with Brown and Leite [51] and decreased negative job behaviors like turnover intentions similar to Yue et al. [12].

5.2Practical implications

Considering the theoretical implications based on the communication channel and information richness theory [13, 27, 31], our findings also have practical implications for organizations and leaders. With the Great Resignation, many organizations had a difficult time recruiting and hiring employees during COVID-19 [52], so preserving positive employee job behaviors will be helpful for the overall operation of the organization, especially under a crisis. First, organizational leaders should understand the proper use of communication tools and choose the right channels [31] since employees utilize multiple channels to collect related information (e.g. [53]). Leaders should know how to utilize multiple communication channels (e.g., email, social media, internal organizational messaging systems, in-person meetings) to make sure the message is delivered to all employees properly [27]. Second, the content of communication should be clear, simple, and frequent, but also be open and honest to provide information [54]. Leaders should provide the right information at the right time and repeat the message as needed, but the content should be clear and simple because employees may not be able to process all information with a limited capacity in a crisis [27, 54]. Lastly, organizational leaders should learn supportive and relational communication [55]. The pandemic caused a crisis in individuals, so each person may have to manage a different level of emotional and physical demands within their personal lives [1]. Organizational support shows a significant positive influence on employees’ well-being [51] and positive job behaviors (e.g. [11, 12]). It is important to embrace the full range of emotions in employees in a crisis, but also be open to listening to their problems and providing guidance [56].

6Conclusion, limitations and future research

6.1Conclusion

This research examined the effects of pre-, during, and post-COVID-19 on accounting professionals’ job behaviors, specifically job performance, job satisfaction, and turnover intentions. Additionally, the moderating effect of organizational communication was considered. Researchers applied quantitative analyses of survey data collected from accounting employees working within the same organization in North Carolina across the time periods. Pairwise t-tests and hierarchical regression analyses were utilized to test the hypotheses. Findings suggest significant differences in job performance between the pre-during and during-post COVID-19 periods. Furthermore, a marginally significant difference in turnover intentions with the during-post COVID-19 period exists. However, statistically significant differences in employee job satisfaction across the periods do not exist. Finally, analyses indicated organizational communication moderates the relationship between the post-COVID-19 period and job performance and turnover intentions, but not job satisfaction. As telework challenges exist and post-COVID-19 staffing concerns continue, organizations must search for and implement ways to enhance organizational communication to encourage increased job performance and decreased employee turnover intentions of accounting professionals.

6.2Limitations

This study has some limitations; therefore, the results should be generalized with caution. First, this study focused on accounting professionals working pre-, during, and post-COVID-19 lockdown restrictions within a single organization in North Carolina. As the pandemic caused millions of employees to resign and find different jobs, employees who switched jobs during the pandemic may show different results and implications than our sample. Second, the study sample focuses on employees in North Carolina. The timelines and restrictions for the pandemic were different across the United States and globally. The results and implications may vary in other studies using data on different occupations or locations. Third, our data was collected in a cross-sectional design, even though the analysis was conducted using a panel design. Employees might respond differently if the data was collected in three different timelines: pre-, during, and post-crisis. Fourth, the number of respondents was considered small at a sample size of 111. However, the statistical analyses used 333 observations since we examined data on each respondent over three time periods. Fifth, the research model control variables were at the employee and organizational levels. In turn, we performed varying statistical analyses to appropriately test our hypotheses. Lastly, this study has a single-source bias, especially for measuring employee performance.

6.3Future research

To address limitations and add insight to the field of study, future research can expand upon the theoretical framework and methodology to add awareness to academic research and practitioner knowledge. First, future studies should consider including employees’ responses who join or quit one organization during the crisis context and compare their responses to whether those who join the organization later show more positive results. Second, future studies could examine job behaviors for accounting professionals working in different states or countries, perhaps with a global organization, and compare the results for generalization. Third, larger sample sizes may be possible with the geographical expansion of future studies. Fourth, future studies should collect data in a panel format, chronologically recording responses over even intervals to observe multiple points in time (e.g., every 2–4 weeks). Fifth, future studies could consider other employee demographics, organizational level characteristics, and work behavior variables to further close the gap in academic research. Lastly, future studies should include more objective measures from multiple sources to avoid single-source bias, such as manager or organizational evaluations or coworker or team performance reviews on employee performance.

Acknowledgments

The authors have no acknowledgments.

Author contributions

CONCEPTION: Dr. Dena Breece, Dr. Stephen Moore, and Dr. SiAhn Mehng.

METHODOLOGY: Dr. Daniel Parisian, Dr. Dena Breece, and Dr. SiAhn Mehng.

DATA COLLECTION: Dr. Dena Breece, Dr. SiAhn Mehng, and Dr. Stephen Moore.

INTERPRETATION OR ANALYSIS OF DATA: Dr. Daniel Parisian and Dr. Dena Breece.

PREPARATION OF THE MANUSCRIPT: Dr. Dena Breece, Dr. SiAhn Mehng, Dr. Daniel Parisian, and Dr. Stephen Moore.

REVISION FOR IMPORTANT INTELLECTUAL CONTENT: Dr. Dena Breece.

SUPERVISION: Dr. Dena Breece.

References

[1] | Abbas J . The impact of coronavirus (SARS-CoV2) epidemic on individuals mental health: The protective measures of Pakistan in managing and sustaining transmissible disease. Psychiatria Danubina. (2020) ;32: (3-4):472–7. |

[2] | Abbas J . Crisis management, transnational healthcare challenges and opportunities: The intersection of COVID-19 pandemic and global mental health. Research in Globalization. (2021) ;3: :100037. |

[3] | Abbas J , Al-Sulaiti K , Lorente DB , Shah SA , Shahzad U . Reset the industry redux through corporate social responsibility: The COVID-19 tourism impact on hospitality firms through business model innovation. In Economic Growth and Environmental Quality in a Post-Pandemic World (2022) (pp. 177–201). Routledge. |

[4] | AICPA. AICPA [Internet]. Available from: https://www.aicpa-cima.com/professional-insights/download/2021-top-issues-commentary-familiar-challenges-in-extraordinary-times. [Accessed 1 October 2022]. |

[5] | Drew J . Journal of Accountancy [Internet]. Available from: https://www.journalofaccountancy.com/issues/2022/feb/attributes-top-performing-firms.html. [Accessed 26 August 2023]. |

[6] | Meyer C . Journal of Accountancy [Internet]. Available from: https://www.journalofaccountancy.com/issues/2022/apr/accounting-firms-hybrid-working.html. [Accessed 15 June 2023]. |

[7] | Tarafdar SS . Financial Management [Internet]. Available from: https://www.fm-magazine.com/news/2021/fun/how-to-develop-and-excel-in-hybrid-workspace.html. [Accessed 15 June 2023]. |

[8] | Maqsood A , Abbas J , Rehman G , Mubeen R . The paradigm shift for educational system continuance in the advent of COVID-19 pandemic: Mental health challenges and reflections. Current Research in Behavioral Sciences. (2021) ;2: :100011. |

[9] | Balsalobre-Lorente D , Abbas J , He C , Pilař L , Shah SA . Tourism, urbanization and natural resources rents matter for environmental sustainability: The leading role of AI and ICT on sustainable development goals in the digital era. Resources Policy. (2023) ;82: :103445. |

[10] | Wang S , Abbas J , Al-Sulati KI , Shah SA . The Impact of Economic Corridor and Tourism on Local Community’s Quality of Life under One Belt One Road Context. Evaluation Review. (2023) :0193841X231182749. |

[11] | Almohtaseb A , Almahameed M , Sharari F , Dabbouri E . The effect of transformation leadership on government employee job satisfaction during Covid-19. Management Science Letters. (2021) ;11: (4):1231–44. |

[12] | Yue CA , Thelen PD , Walden J . How empathetic leadership communication mitigates employees' turnover intention during COVID-19-related organizational change. Management Decision. (2023) ;61: (5):1413–33. |

[13] | Daft RL , Lengel RH . Organizational information requirements, media richness and structural design. Management Science. (1986) ;32: (5):554–71. |

[14] | Iacurci G . CNBC [Internet]. Available from: https://www.cnbc.com/2023/02/01/why-2022-was-the-real-year-of-the-great-resignation.html#:∼:text=Investing%20Club-,2022%20was%20the%20’real%20year,the%20Great%20Resignation%2C’%20says%20economist&text=About%2050.5%20million%20people%20quit,known%20as%20the%20Great%20Resignation. [Accessed 9 June 2023]. |

[15] | Miller D , Yamada H . ABC News Network [Internet]. Available from: https://abcnews.go.com/US/great-resignation-origins-means-future-business/story?id=84222583. [Accessed 9 June 2023]. |

[16] | Cleveland Clinic. Cleveland Clinic [Internet]. Available from: https://health.clevelandclinic.org/when-to-leave-a-job/. [Accessed 9 June 2023]. |

[17] | Kimbrough K . LinkedIn [Internet]. Available from: https://www.linkedin.com/pulse/what-world-work-look-like-2022-expect-employees-remain-kimbrough/. [Accessed 9 June 2023]. |

[18] | Robinson B . Forbes [Internet]. Available from: https://www.forbes.com/sites/bryanrobinson/2022/12/01/5-reasons-for-boomerang-employees-and-the-great-regret-in-employment/?sh=48b9512e6092. [Accessed 9 June 2023]. |

[19] | Klotz AC , Bolino MC . Harvard Business Review [Internet]. Available from: https://hbr.org/2022/09/when-quiet-quitting-is-worse-than-the-real-thing. [Accessed 9 June 2023]. |

[20] | Newman A , Eva N , Bindl UK , Stoverink AC . Organizational and vocational behavior in times of crisis: A review of empirical work undertaken during the COVID-19 pandemic and introduction to the special issue. Applied Psychology. (2022) ;71: (3):743–64. |

[21] | Vaziri H , Casper WJ , Wayne JH , Matthews RA . Changes to the work–family interface during the COVID-19 pandemic: Examining predictors and implications using latent transition analysis. Journal of Applied Psychology. (2020) ;105: (10):1073. |

[22] | Yuan Z , Ye Z , Zhong M . Plug back into work, safely: Job reattachment, leader safety commitment, and job engagement in the COVID-19 pandemic. Journal of Applied Psychology. (2021) ;106: (1):62–70. DOI: 10.1037/ap10000860 |

[23] | Fu SQ , Greco LM , Lennard AC , Dimotakis N . Anxiety responses to the unfolding COVID-19 crisis: Patterns of change in the experience of prolonged exposure to stressors. Journal of Applied Psychology. (2021) ;106: (1):48–61. DOI: 10.1037/ap10000855. |

[24] | Ployhart RE , Shepherd WJ , Strizver SD . The COVID-19 pandemic and new hire engagement: Relationships with unemployment rates, state restrictions, and organizational tenure. Journal of Applied Psychology. (2021) ;106: (4):518–529. DOI: 10.1037/ap10000917. |

[25] | Bajrami DD , Terzic A , Petrovic M , Radovanovic M , Tretiakova TN , Hadoud A . Will we have the same employees in hospitality after all? The impact of COVID-19 on employee’s work attitudes and turnover intentions. International Journal of Hospitality Management. (2021) ;94: :102754. DOI: 10.1016/j.ijhm.2020.102754 |

[26] | Syrek C , Kuhnel J , Vahle-Hinz T , Bloom J . Being an accountant, cook, entertainer and teacher – all at the same time: Changes in employees’ work and work-related well-being during the coronavirus (COVID-19) pandemic. International Journal of Psychology. (2022) ;57: (1):20–32. DOI: 10.1002/ijo12761 |

[27] | Daft RL . The leadership experience. Cengage Learning. (2023) . |

[28] | Kaplan S , Engelsted L , Lei X , Lockwood K . Unpackaging manager mistrust in allowing telework: Comparing and integrating theoretical perspectives. Journal of Business and Psychology. (2018) ;33: :365–82. |

[29] | Bernstein E , Blunden H , Brodsky A , Sohn W , Waber B . Harvard Business Review [Internet]. Available from: https://hbr.org/2020/07/the-implications-of-working-without-an-office. [Accessed 22 May 2023]. |

[30] | Stephens KK , Jahn JL , Fox S , Charoensap-Kelly P , Mitra R , Sutton J , Waters ED , Xie B , Meisenbach RJ . Collective sensemaking around COVID-19: Experiences, concerns, and agendas for our rapidly changing organizational lives. Management Communication Quarterly. (2020) ;34: (3):426–57. |

[31] | Lengel RH , Daft RL . The selection of communication media as an executive skill. Academy of Management Perspectives. (1988) ;2: (3):225–32. |

[32] | Sanders K , Nguyen P , Bouckenooghe D , Rafferty A , Schwartz G . Unraveling the what and how of organizational communication to employees during the COVID-19 pandemic: Adopting an attributional lens. The Journal of Applied Behavioral Science. (2020) ;56: (3):289–293. DOI: 10.1177/0021886320937026 |

[33] | DeFilippis E , Impink SM , Singell M , Polzer JT , Sadun R . Collaborating during coronavirus: The impact of COVID-19 on the nature of work. National Bureau of Economic Research; (2020) Aug 3. |

[34] | Handy C . Trust and the virtual organization. Harvard Business Review. (1995) ; May-June: 40–50. |

[35] | Ahmed T , Khan M , Duangkamol T , Siraphatthada Y , Phumdara T . Impact of employees engagement and knowledge sharing on organizational performance: Study of HR challenges in COVID-19 pandemic. Human Systems Management. (2020) ;39: (4):589–601. DOI: 10.3233/HSM-201052 |

[36] | Soomro SA . Nexus between perceived job insecurity and employee work-related outcomes amid COVID-19: Attenuating effect of supervisor support. Human Systems Management. (2022) ;41: (2):199–209. DOI: 10.3233/HSM-201150 |

[37] | Stephenson J , Vaganay M , Coon D , Cameron R , Hewitt N . The role of Facebook and Twitter as organisational communication platforms in relation to flood events in Northern Ireland. Journal of Flood Risk Management. (2018) ;11: (3):339–50. |

[38] | McKinsey & Company. McKinsey & Company [Internet]. Available from: https://www.mckinsey.com/featured-insights/coronavirus-leading-through-the-crisis/covid-19-where-weve-been-where-we-are-and-where-were-going. [Accessed 10 June 2023]. |

[39] | Bailey K , Breslin D . The COVID-19 pandemic: What can we learn from past research in organizations and management? International Journal of Management Reviews. (2021) ;23: (1):3–6. |

[40] | NCDHHS. NCDHHS [Internet]. Available from: https://www.ncdhhs.gov/news/press-releases/2020/03/27/governor-cooper-announces-statewide-stay-home-order-until-april-29#:∼:text=Governor%20Roy%20Cooper%20ordered%20people,of%20gatherings%20to%2010%20people. [Assessed 1 May 2023]. |

[41] | NC Governor Roy Cooper. NC Governor Roy Cooper [Internet]. Available from: https://governor.nc.gov/news/press-releases/2021/04/21/governor-cooper-outlines-timeline-lifting-states-covid-19-restrictions. [Assessed 1 February 2023]. |

[42] | Spector P . Job Satisfaction. Thousand Oaks (CA): Sage; (1997) . P. 75–76. |

[43] | Yousef DA . Organizational commitment: A mediator of the relationship leadership behavior with job satisfaction and performance in a non-western country. Journal of Managerial Psychology. (2000) ;15: (1):6–24. DOI: 10.1108/02683940010305270 |

[44] | Vermeir P , Blot S , Degroote S , Vandijck D , Mariman A , Vanacker T , Peleman R , Verhaeghe R , Vogelaers D . Communication satisfaction and job satisfaction among critical care nurses and their impact on burnout and intention to leave: A questionnaire study. Intensive and Critical Care Nursing. (2018) ;48: :21–7. |

[45] | Van Veldhoven MJPM , Meijman T . Het meten van psychosociale arbeidsbelasting met een vragenlijst: De vragenlijst beleving en beoordeling van de arbeid (VBBA). (1994) . |

[46] | Penley LE , Hawkins B . Studying interpersonal communication in organizations: A leadership application. Academy of Management Journal. (1985) ;28: (2):309–326. DOI: 10.5465/256203. |

[47] | Taber KS . The use of Cronbach’s alpha when developing and reporting research instruments in science education. Research in Science Education. (2018) ;48: :1273–96. |

[48] | Helm R , Mark A . Analysis and evaluation of moderator effects in regression models: State of art, alternatives and empirical example. Review of Managerial Science. (2012) ;6: :307–32. |

[49] | Chen J , Silverthorne C , Hung J . Organization communication, job stress, organizational commitment, and job performance of accounting professionals in Taiwan and America. Leadership and Organizational Development Journal. (2005) ;27: (4):242–249. DOI: 10.1108/01437730610666000 |

[50] | Vyas L . “New normal” at work in a post-COVID world: Work–life balance and labor markets. Policy and Society. (2022) ;41: (1):155–67. |

[51] | Brown A , Leite AC . The effects of social and organizational connectedness on employee well-being and remote working experiences during the COVID-19 pandemic. Journal of Applied Social Psychology. (2023) ;53: (2):134–52. |

[52] | Bakertilly. Bakertilly. [Internet]. Available from https://www.bakertilly.com/insights/recruiting-and-hiring-challenges-during-the-covid-19-pandemic [Accessed 22 September 2023]. |

[53] | Yu S , Abbas J , Draghici A , Negulescu OH , Ain NU . Social media application as a new paradigm for business communication: The role of COVID-19 knowledge, social distancing, and preventive attitudes. Frontiers in Psychology. (2022) ;13. DOI: 10.3389/fpsyg.2022.903082. |

[54] | Mendy A , Stewart ML , Van Akin K . McKinsey & Company. [Internet] Available at: https://www.mckinsey.com/capabilities/people-and-organizational-performance/our-insights/a-leaders-guide-communicating-with-teams-stakeholders-and-communities-during-covid-19#/ [Accessed 22 September 2023] |

[55] | Hasson B , Bagley P , Eller K . Journal of Accountancy. Available from: https://www.journalofaccountancy.com/issues/2023/apr/how-remote-work-affected-early-caree-auditors.html [Accessed 22 September 2023]. |

[56] | Martin S . Center for Creative Leadership. [Internet] Available from: https://www.ccl.org/articles/leading-effectively-articles/communicating-in-a-crisis-what-when-and-how/ [Accessed 22 September 2023]. |