Research on enterprise digital transformation disclosure based on hypocrisy theory

Abstract

By using the interactive big data between enterprises and stakeholders in social media, this paper investigates the views of different stakeholders on the disclosure of enterprise digital transformation. In view of the social media platform brings together different stakeholders, this paper uses the organizational hypocrisy theory to explore the stakeholders’ Reflection on the hypocritical speech, decision-making and action strategies adopted in the disclosure of enterprise digital transformation. Through data mining and computer-aided emotion analysis, the posts of sina Weibo’s top 500 Chinese enterprises from December 31, 2020 to December 31, 2021 and the reactions of stakeholders are retrieved and analyzed. It is found that stakeholders have different reactions to the hypocrisy strategies of enterprises. Although stakeholders pay more attention to information related to actions, and the disclosure of such actions will cause positive and negative reactions, the inconsistency of speech and decision-making will produce positive reactions and reduce negative impressions. Overall, research shows that the use of organizational hypocrisy strategies in social media can enable enterprises to manage the views and legitimacy of stakeholders.

1Introduction

Corporate scandals around the world continuously threaten the legitimacy and trust of organizations. In the current media-driven environment, if an enterprise’s behavior does not meet its claimed standards of social responsibility, it will be regarded as hypocrisy [1]. In particular, the COVID-19 pandemic severely affects international economic development. With the normalization of epidemic prevention and control, it is foreseeable that stakeholders will become more sensitive to corporate hypocrisy and react strongly, such as withdrawing financial and material support. Moreover, organizations that lack legitimacy and trust for a long time are bound to affect social and economic development [2].

In recent years, scholars have shown a keen interest in corporate hypocrisy. For example, Brunsson proposed that organizational hypocrisy, different from intentional fraud, is a management reality in a complex environment [3]. Organizational hypocrisy is considered an inconsistency between words and actions at the level of behavior [4]. On the one hand, influenced by the complexity of the environment, there is no certain “rule” for enterprise operation to follow, and on the other hand, when establishing organizational positioning and development goals, managers have to face different opinions and values from stakeholders, which sometimes even conflict with each other [5], for instance, economic benefits often differ from environmental or social benefits [6]. The ultimate goal of corporate behavior is to realize strategic goals [7], and enterprises guarantee the legitimacy of different stakeholders through these “symbolic ambiguity” behaviors that are deliberately expressed and different from the organizational reality [8].

Driven by digital technological development, Digital Transformation (DT) is widely regarded as a strategic measure to improve service performance, enhance customer experience, innovate business models, practice corporate social responsibility, and cope with the impact of COVID-19 [9]. Among a lot of information publicly disclosed by enterprises, digital transformation has become a hot topic concerned by stakeholders. Relevant research results reveal that, similar to informatization transformation, technology is only one of many difficulties that enterprises must solve to maintain competitiveness in the digital world [10]. Besides, they should also carry out value remolding in organizational structure, business process, and public relations management [11]. Although people have high expectations for DT, there is still a lack of comprehensive understanding of this phenomenon, especially stakeholders’ views on the digital transformation of enterprises and the resulting social responsibility impact. Previous studies on corporate information disclosure often imply a prerequisite, that is, enterprises affect the perception of stakeholders through selective information disclosure to obtain legitimacy [12]. This study pays special attention to enterprises’ digital transformation information disclosure on social media. As a set of online applications that can enable users to create and share content, social media thoroughly changed the way that the public communicates with enterprises. Meanwhile, it is one of the most important channels of information dissemination, shows great value in promoting public participation [13], and provides an ideal big data environment for studying the interaction between enterprises and stakeholders. Digital transformation is an important strategic measure for enterprises to cope with the destructive innovation of digital technology. It is not only a remolding of enterprise management and competitive advantages but also an important way to practice corporate social responsibility, which requires stakeholders’ participation and support. This study utilizes the big data of the interaction between enterprises and stakeholders in social media and introduces the theory of organizational hypocrisy to investigate stakeholders’ reactions to enterprises’ digital transformation disclosure strategy. The study focuses on the correlation between disclosure of a firm’s actions, words and decisions and stakeholders’ interactive responses to their doings, exploring the legitimacy of a firm’s strategy to maintain a stakeholder perspective through a combination ofdisclosures.

2Theoretical framework

At present, there is no connotation and definition of organizational hypocrisy that is universally recognized by scholars. Based on the literature review of business management and social psychology, this paper summarizes the connotation of two different levels of organizational hypocrisy from the perspective of perception, that is, moral hypocrisy and behavioral hypocrisy. This study focuses on the behavioral hypocrisy of organizational hypocrisy and its impact (Table 1).

Table 1

Two aspects of connotation of organizational hypocrisy

| Moral hypocrisy | Behavioral hypocrisy | |

| Definition | [Enterprises] try to appear more noble than they really are | (Enterprises’) External actions are not consistent with what they claim |

| Representative scholar | Monin (2011) | Brunsson (2007) |

| Key point of concept | Fraudulent conduct | Action does not consistent with words |

| Representative viewpoint | [Enterprises] pretend to be morally superior | What enterprises claim is inconsistent with actions |

Moral hypocrisy, which refers to an enterprise’s attempt to appear nobler than it actually is, is often regarded as having ulterior motives or greed [14]. In contrast, corporate hypocrisy at the behavioral level refers to the inconsistency between what an enterprise declares and its actions, which reflects the deviation from its words to its decisions and actions [15]. Different from moral hypocrisy, behavioral hypocrisy does not involve ethical and moral issues [16]. The nature of behavioral hypocrisy does not originate from malice, but it affects the perception of stakeholders and weakens the reliability and predictability of the organization. Therefore, if enterprise managers try to maintain the legitimacy of different stakeholders, they will often adopt a variety of external behavior to meet their needs.

The divergence among different stakeholder groups of the organization is the basis of the theoretical framework of this study. Modern enterprises often have to face multiple stakeholders with different values and demands, and sometimes their demands even conflict with each other, which often makes enterprise managers fall into a dilemma. What is legitimate for some stakeholders may well be the opposite for others. Neu et al. proposed that when the economic interests of an enterprise conflict with the environmental protection benefits, the enterprise should disclose as little environmental protection information as possible, so as to dilute the environmental protection claims of some stakeholders [17]. In contrast, Brunsson pointed out that organizational hypocrisy helps to maintain enterprises’ legitimacy among different stakeholders. Speech, decision, and action are three important forms of the external behavior of an organization, which are one-way correlated with each other [18]. Lipson further explained Brunsson’s view that speech and decision can compensate for the consequences caused by inconsistent actions, while actions can compensate for the negative effects of inconsistent speech and decision, and this relationship is called “anti-coupling” [19]. Under the theoretical framework of organizational hypocrisy, managers can assign different “relevant values” to the speech, decision, and action of the enterprise. In other words, when maintaining the legitimacy of different stakeholder groups, enterprises do not disclose information as little as possible but weaken the negative impact brought by inconsistent action disclosure through speech and decision disclosure. Organization hypocrisy provides a completely new way for enterprises to maintain different stakeholder groups, so that managers can ensure the legitimacy of the groups of different stakeholders (e.g., talking about their core appeal or releasing the related decisions) at low cost, and centralize the core resources on actions that are closely related to the organization’s strategic objectives, in order to meet the core stakeholders.

Studies have shown that, compared with the disclosure of ongoing or completed actions, enterprises are more inclined to disclose information about the future [20]. As the disclosure of actions can be verified, it is often considered to have high credibility by the audience [21]. After analyzing the sustainability reports disclosed by the Top 500 US enterprises, Brown et al. found that high-quality action disclosure only has a positive impact on the reputation perception of enterprises with good operating conditions [22]. The COVID-19 pandemic poses a significant challenge to traditional ways of disseminating corporate information. With the new generation of information technology as the main driving force, the digital wave is booming, which injects new vitality into the sustainable development of enterprises. Currently, digital transformation has become the consensus of all enterprises and industries, which is the key strategy for enterprises to actively respond to digital transformation, enhance competitiveness, and practice corporate social responsibility. Based on this, this study proposes the following hypotheses:

H1a. The action disclosure of enterprises’ digital transformation is positively correlated with the participation of stakeholders

Relatively speaking, according to Brunsson’s organizational hypocrisy theory, due to the divergent demands of stakeholder groups, enterprises’ action disclosure of a certain stakeholder group is likely to lead to negative reactions from another group [23]. Given that there are many different stakeholder groups in the social media environment, the disclosure of an enterprise’s actions will cause negative reactions. Therefore, the following hypotheses are proposed:

H1b. The disclosure of enterprises’ actions in digital transformation is negatively correlated with the participation of stakeholders

Previous research on CSR information disclosure shows that the speech and decision disclosure is correlated with the positive perception of stakeholders. Bansal’s study confirmed that enterprises with a low level of environmental governance can reduce non-systemic risk through disclosure of environmental commitment, which reflects stakeholders’ concern about disclosure of corporate speech and decisions. Cho and Guidry et al., by using an archiving method, found that the quality of environmental information disclosure of enterprises is positively correlated with environmental reputation evaluation and Dow Jones Sustainability Index, even if the actual environmental performance of enterprises is not good, which reflects that corporate reputation is driven more by “what they say” rather than “what they do”. Stakeholders believe that the remarks disclosed by enterprises are the prediction of their actions [24]. Brunsson’s organizational hypocrisy model assumes that there will always be some stakeholders who question enterprises’ actions. Therefore, when the legitimacy of stakeholders is at risk (i.e., negative reflection), managers should use speech and decision-making disclosure to alleviate their concerns. If the hypocrisy model is true, the disclosure of corporate actions is correlated with positive and negative reactions, while speech and decision disclosure tend to stimulate stakeholders’ positive reactions, and can even reduce the negative reactions to action disclosure. Therefore, enterprises can maintain the legitimacy of different stakeholder groups simultaneously. Based on this, the following hypotheses are proposed:

H2. The speech and decision disclosure of enterprises’ digital transformation is positively correlated with the participation of stakeholders

Speech and decision disclosure, which is usually correlated with corporate vision and goal, is a qualitative soft evaluation. While action disclosure is related to results and achievements, and is usually a quantitative hard evaluation. On the one hand, disclosure of speech, decision and action will affect the perception of stakeholders to a certain extent. The intensity of stakeholders’ reaction to speech and decision disclosure may be different from that of action disclosure. Toms believes that when an enterprise changes from non-disclosure commitment to disclosure, general wording and content can significantly improve the reputation of the enterprise [25]. After that, additional disclosures of speech and decisions will have no reputational impact until companies begin to disclose detailed implementation of policies and objectives and quantitative monitoring evaluations. Therefore, compared with the perception of disclosure of speech and decision, stakeholders have a greater reaction to disclosure of action. In view of this, the following hypotheses are proposed in this study:

H3. Compared with speech and decision disclosure of enterprise digital transformation, stakeholders reflect more on the disclosure of action

3Research method

3.1Data collection

This study aims to investigate the relationship between digital transformation disclosure and stakeholder response in different types of companies, mainly through Python crawler technology to mine the big data of interaction between China’s top 500 listed companies and their stakeholders on Sina Weibo. Sina Weibo is one of the most popular social media websites in China, with 510 million active users and 224 million daily active users as of September 2020 (Sina, 2020). Therefore, Sina Weibo is not only a communication medium between enterprises and stakeholders but also a big data platform that gathers different stakeholders and analyzes their behavior patterns. Besides, posts on Sina Weibo are also limited to 140 characters, as on microblogging sites such as Twitter, while the use of emoticons reveals users’ specific views [26]. In this study, subscribers who follow enterprises on Sina Weibo are regarded as their stakeholders. China’s top 500 listed companies list in 2021 comes from Fortune China (https://www.caifuzhongwen.com/fortune500/). On the one hand, China’s top 500 listed companies are more active in digital transformation and have high visibility, and on the other hand, compared with small enterprises, top 500 enterprises have a large number of stakeholders and invest more in social media than small and medium-sized enterprises [27].

3.2Coding sampling

In this study, the posts on digital transformation actually disclosed by enterprises and the real reactions of stakeholders to the posts were studied, and the posts on enterprise informatization transformation were manually divided into three categories, namely, speech disclosure, decision disclosure, and action disclosure, for analysis.

Of the 500 enterprises, only 19 have released specialized posts on digital transformation. According to the standard industry classification, these enterprise types include industry, general trade, securities industry, Internet services, and commercial banking. The criteria for judging whether a post is relevant to digital transformation are title and content. If the title or content theme of a post contains terms related to digital transformation, such as digital technology, technological change, digital economy, digital value-added, digital workshop, etc., it will be considered a post about enterprise digital transformation disclosure. In this study, construction-monthly sampling was adopted, which was similar to construction-weekly sampling, to carry out code sampling of 630 posts. Later, the random number generator was used to select the sampling date to build the construction month, and specify the number of each month, for example, May 2021 is “1”, June 2021 is “2”, July 2021 is “3”, and so on. Finally, a day of a month was selected randomly to build the full date. If “1” is selected randomly in the first month, May 1, 2021 will be the selection date. For the second month, if “12” is randomly selected, all post codes of the selected date December 12, 2021 will be available. If no post is published on the selected date, the next date with post will be included in the study example.

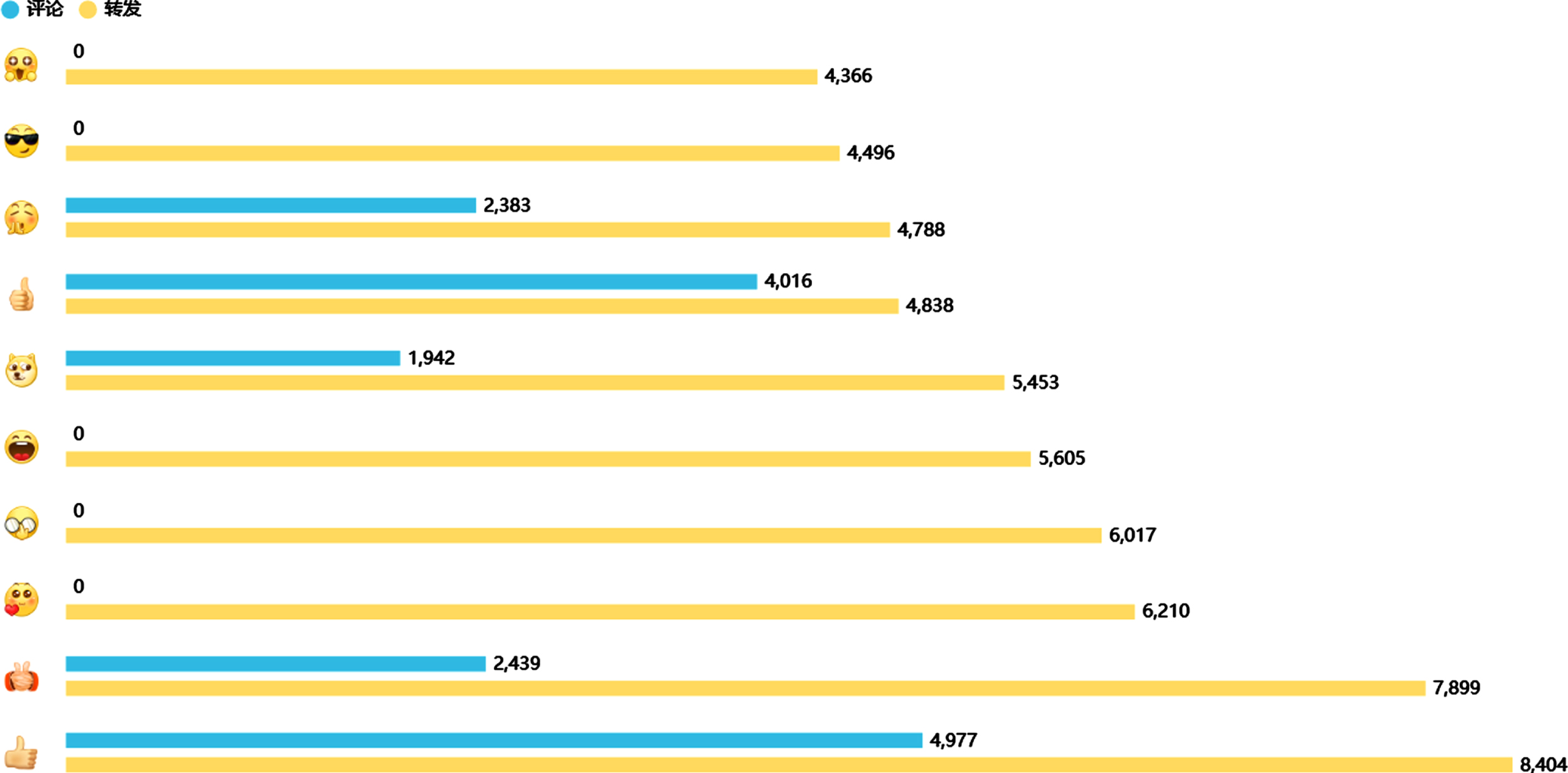

Fig. 1

Distribution of emoticon usage.

3.3Variable coding

A code book is prepared to analyze the post strategies of enterprises disclosing digital transformation on Sina Weibo. An initial classification set is established under the main variables, such as three different types of hypocritical disclosure of digital transformation posts, and stakeholder engagement. Then, the method of induction is adopted to appropriately add or revise the classification criteria by reading the posts on digital transformation to ensure that the classification is accurate enough. Variables directly affect the creation of first-level codes, which define stakeholder participation in enterprise digital transformation posts as the degree of interaction, and then measure it by the number of general reactions (likes, shares, and comments) and special reactions of enterprise digital transformation disclosure posts [28]. The degree of interaction represents stakeholders’ interest in information disclosure of digital transformation [29]. In the study, 632 posts on enterprise digital transformation were hand-coded and classified into three hypocritical disclosure strategies, namely speech, decision, and action disclosure. If a disclosure subject exists in a post, it will be coded as “1”, otherwise, it will be “0”. The top five emojis that appeared in replies to posts are “Love”, “Great”, “Wow”, “Interesting”, and “Angry”.

Referring to the study of Saxton et al., some control variables were proposed based on the characteristics of posts, and then the logarithm of the number of characters (Character_log) in each post was used to control the amount of information interacting with stakeholders. Social psychology researchers hold that longer texts are more persuasive than shorter ones. Then, dummy variables were created for each hyperlink (URL), hashtag, image, and video contained in the post. Hyperlinks can take users to external web pages for additional information, so stakeholders can make more informed decisions about whether and how to react to that post, while hashtags can trigger public discussion on a certain topic and improve audience responsiveness [30]. Visual content can present more valuable corporate information to stakeholders [31], and it has a stronger framing effect on stakeholders’ attitudes than text [32]. Moreover, in this study, the size of enterprises was also controlled, because large enterprises may attract more diverse demands and reactions [33]. The natural logarithmic transformation of the quarterly total assets of the firm is used as a proxy for firm size, and all models include fixed effects to consider time-invariant and unobservable firm-level factors, as well as time fixed-effects (weeks) to eliminate time-trend effects.

The message format is defined as the form in which the enterprise displays information. According to Waters et al., five different multimedia category patterns were created, including links, photos, graphics, video or audio files, as well as a text-only category [34]. These message formats are encoded as presence (1) or absence (0).

3.3.1Coding training

To improve the reliability of the encoder, two graduate students majoring in business administration with similar majors in this research field were selected as coders to explain the concept and evaluation criteria of each variable to ensure that the coders understand the meaning of the variables. Before formal coding, 60 coding samples were tested, and two coders were asked to code separately and correct the coding results. The above steps were repeated until all the results satisfied the research requirements. Later, the Holsti formula was used for reliability spot check, and the results showed that the Holsti reliability was 95.3%, indicating that the coding reliability was reliable. Besides, Krippendorf’s alpha value was 0.85 (critical value: 0.80) and Scott’s Pi reliability was 0.85 (critical value: 0.60), both of which were higher than the critical values.

3.3.2Model specifications

To verify the hypothesis, the negative binomial regression model was adopted in this study, and the reasons are as follows: first of all, the counting of the results of this study is the frequency of occurrence of discrete distribution; Secondly, the counting variance of the dependent variable is greater than the mean, so excessive dispersion needs to be adjusted. As the negative binomial regression requires a logarithmic transformation of the dependent variable, the regression coefficients need to be exponential in order to interpret the results. Then the following model was proposed to verify H1a, H1b, and H2:

(1)

To test H3, speech and decision disclosure were selected as the benchmark level to compare the impact of action disclosure on stakeholders’ reactions and propose the following model:

(2)

Where log(y) is the dependent variable of stakeholders’ reactions, including general reactions (likes, shares, and comments) and specific reactions (expressions of “Love, Great, Wow, Interesting, and Angry”, as well as positive or negative comments). reactions to specific stakeholders were further measured by creating dummy variables for expressions of “Love, Great, Wow, Interesting, and Angry” and the effect (positive, negative, or neutral) of comments. The value will be assigned to “1” if the post receives at least one comment with a specific expression or one positive or negative comment (PosComment and NegComment), otherwise, it will be “0”. ThenJieba sentiment analysis was performed to calculate the net sentiment score of each individual comment [35] and determine whether there was at least one positive or negative comment for each post. Besides, if the post has action disclosure, it will be coded as “1”, and if it does not, it will be “0”. Similarly, it will be set as “1” if the post has speech disclosure, otherwise, it will be set as “0”. If a post has decision disclosure, it will be coded as “1”, otherwise, it will be “0”. The variables involved in this study and their measurements are shown in Table 2.

Table 2

Measurement of variables

| Name of variable | Definition | |

| Stakeholders’ reactions | ||

| Likes | Likes | Total number of likes per post |

| Shares | Shares | Total Shares per post |

| Comments | Comments | Total Comments per post |

| Love | Love | If the comments on a post contain at least one emoji of Love, then the dummy variable is 1, otherwise it is 0 |

| Great | Great | If the comments on a post contain at least one emoji of Wow, then the dummy variable is 1, otherwise it is 0 |

| Wow | Wow | If the comments on a post contain at least one emoji of Haha, then the dummy variable is 1, otherwise it is 0 |

| Interesting | Interesting | If the comments on a post contain at least one emoji of Interesting, then the dummy variable is 1, otherwise it is 0 |

| Angry | Angry | If the comments on a post contain at least one emoji of Angry, then the dummy variable is 1, otherwise it is 0 |

| Positive comment | PosComments | If the comments on a post contain at least one positive comment, then the dummy variable is 1, otherwise it is 0 |

| Negative comment | NegComments | If the comments on a post contain at least one negative comment, then the dummy variable is 1, otherwise it is 0 |

| Independent variable | ||

| Action disclosure | Act | If the post discloses action information, the dummy variable is 1, otherwise, it is 0 |

| Speech disclosure | Talk | If the post discloses speech information, the dummy variable is 1, otherwise, it is 0 |

| Decision disclosure | Decision | If the post discloses decision information, the dummy variable is 1, otherwise, it is 0 |

| Control variable | ||

| Text length | Wordcount | Log conversion of the number of characters (excluding Spaces) in a post |

| Use of photos | Url | The dummy variable is equal to 1 if the post contains hyperlinks (i.e., “http://”), otherwise, it is 0 |

| Use of hyperlink | Photo | The dummy variable is 1 if the post contains photos, otherwise, it is 0 |

| Use of photos | Video | The dummy variable is 1 if the post contains videos, otherwise, it is 0 |

| Enterprise scale | Firm | Logarithmic conversion of a firm’s quarterly total assets |

4Research results

4.1Descriptive statistics and correlation analysis

Among 632 posts on digital transformation disclosure, 1031 likes (SD = 7294, Mdn = 42), 104 shares (SD = 1409, Mdn = 5.0, and 47 comments (SD = 368, Mdn = 1) were received on average. In the specific reflection of stakeholders, the posts receiving emotional reactions account for a lower proportion, less than half, including “Love” (41%), “Great” (26%), “Wow” (24%), “Interesting” (7%), and “Angry” (5%). About 63% of the posts generated at least one positive comment and 32% received at least one negative comment in terms of the mood of the comment. Although positive comments were more common than negative ones, more than one-third of posts received at least one negative comment, indicating that stakeholders had different views on corporate disclosure. As for the hypocritical strategies of enterprise digital transformation, 7% of the posts adopted action disclosure, 24% adopted speech disclosure, and 4% adopted decision disclosure, indicating that enterprises adopted speech disclosure more than action disclosure to communicate with stakeholders on enterprise digital transformation. The average number of words per post about the control variable is 122 characters, which is close to the 140-character threshold. In terms of the multimedia nature of posts, 45% included a hyperlink that took users to an external web page, 51% included photos, and 19% included videos. Table 3 shows the reactions of different stakeholders and Pearson correlation analysis. The results show that most of the hypocritical strategies of digital transformation are significantly correlated with stakeholder reactions. The highest VIF is 1.19, indicating that there is no multicollinearity problem.

Table 3

Descriptive statistics

| Quantity | Mean | SD | Min | Max | |

| Stakeholders’ general reactions | |||||

| Likes | 632 | 1182.21 | 10598.36 | 0 | 423450 |

| Shares | 632 | 179.34 | 1600.76 | 0 | 92790 |

| Comments | 632 | 51.3 | 417.69 | 0 | 34045 |

| Stakeholders’ special reactions | |||||

| Love | 632 | 0.643 | 0.446 | 0 | 0 |

| Great | 632 | 0.356 | 0.476 | 0 | 0 |

| Wow | 632 | 0.216 | 0.409 | 0 | 0 |

| Interesting | 632 | 0.234 | 0.411 | 0 | 0 |

| Angry | 632 | 0.121 | 0.321 | 0 | 0 |

| Positive comment | 632 | 0.616 | 0.592 | 0 | 0 |

| Negative comment | 632 | 0.416 | 0.607 | 0 | 0 |

| Independent variable | |||||

| Action disclosure | 632 | 0.08 | 0.93 | 0 | 0 |

| Speech disclosure | 632 | 0.24 | 1.06 | 0 | 0 |

| Decision disclosure | 632 | 0.02 | 0.82 | 0 | 0 |

| Control variable | |||||

| Text length | 632 | 4.71 | 1.211 | 4.687 | 8.654 |

| Use of photos | 632 | 0.43 | 0.581 | 0 | 0 |

| Use of hyperlink | 632 | 0.34 | 0.621 | 0 | 0 |

| Use of photos | 632 | 0.23 | 0.601 | 0 | 0 |

| Enterprise scale | 632 | 9.79 | 1.141 | 9.124 | 13.45 |

Table 4

Correlation coefficient matrix

| Number | Variable | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| 1 | Likes | 1 | ||||||||

| 2 | Shares | 0.309*** | 1 | |||||||

| 3 | Comments | 0.247*** | 0.608*** | 1 | ||||||

| 4 | Love | 0.069*** | 0.075*** | 0.078*** | 1 | |||||

| 5 | Great | 0.119*** | 0.119*** | 0.129*** | 0.437*** | 1 | ||||

| 6 | Wow | 0.167*** | 0.164*** | 0.178*** | 0.339*** | 0.419*** | 1 | |||

| 7 | Interesting | 0.204*** | 0.201*** | 0.215*** | 0.216*** | 0.339*** | 0.419*** | 1 | ||

| 8 | Angry | 0.132*** | 0.129*** | 0.159*** | 0.236*** | 0.265*** | 0.381*** | 0.365*** | 1 | |

| 9 | Positive comment | 0.067*** | 0.079*** | 0.087*** | 0.436*** | 0.405*** | 0.349*** | 0.240*** | 0.316*** | 1 |

| 10 | Negative comment | 0.103*** | 0.109*** | 0.129*** | 0.330*** | 0.373*** | 0.427*** | 0.329*** | 0.449*** | 0.513*** |

| 11 | Action disclosure | 0.027*** | –0.005 | –0.01 | 0.028*** | 0.022*** | –0.004 | 0.032*** | 0.003 | 0.005 |

| 12 | Speech disclosure | –0.035*** | –0.041*** | –0.062*** | –0.071*** | –0.137*** | –0.148*** | –0.086*** | –0.126*** | –0.137*** |

| 13 | Decision disclosure | 0.010 | –0.009 | –0.015* | –0.035*** | –0.037*** | –0.038*** | –0.020** | –0.019** | –0.047*** |

| 14 | Text length | 0.006 | –0.019** | –0.013 | –0.067*** | –0.032*** | –0.051*** | –0.023*** | –0.075*** | –0.042*** |

| 15 | Use of photos | 0.036*** | 0.048*** | 0.054*** | 0.136*** | 0.126*** | 0.115*** | 0.062*** | 0.050*** | 0.129*** |

| 16 | Use of hyperlink | 0.007 | –0.030*** | –0.027*** | –0.086*** | –0.035*** | –0.071*** | –0.064*** | –0.122*** | –0.087*** |

| 17 | Use of photos | 0.020** | 0.009 | 0.009 | –0.069*** | –0.092*** | –0.036*** | –0.016* | –0.035*** | –0.089*** |

| 18 | Enterprise scale | 0.034*** | –0.017** | 0.00 | 0.092*** | –0.005 | 0.035*** | 0.008 | 0.113*** | 0.158*** |

| Number | Variable | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 |

| 1 | Likes | |||||||||

| 2 | Shares | |||||||||

| 3 | Comments | |||||||||

| 4 | Love | |||||||||

| 5 | Great | |||||||||

| 6 | Wow | |||||||||

| 7 | Interesting | |||||||||

| 8 | Angry | |||||||||

| 9 | Positive comment | |||||||||

| 10 | Negative comment | 1 | ||||||||

| 11 | Action disclosure | –0.01 | 1 | |||||||

| 12 | Speech disclosure | –0.176*** | –0.163*** | 1 | ||||||

| 13 | Decision disclosure | –0.037*** | –0.058*** | –0.096*** | 1 | |||||

| 14 | Text length | –0.054*** | 0.134*** | 0.167*** | 0.083*** | 1 | ||||

| 15 | Use of photos | 0.108*** | 0.023*** | –0.064*** | –0.037*** | –0.013* | 1 | |||

| 16 | Use of hyperlink | –0.112*** | –0.025** | 0.002 | 0.015* | 0.252*** | 0.058*** | 1 | ||

| 17 | Use of photos | –0.078*** | 0.036 | 0.075*** | 0.021** | 0.150*** | 0.097*** | 0 | 1 | |

| 18 | Enterprise scale | 0.126 | 0.007 | –0.004 | 0.020** | 0.003 | 0.072*** | –0.077*** | –0.021** | 1 |

4.2Multivariate analysis

Logit regression results were used to verify hypothesis H1. The analysis of stakeholders’ likes shows that action disclosure is a hypocritical variable that is significantly correlated with Likes. The results showed that stakeholders would only generally approve action disclosure. To explain the effect of this hypocritical strategy on Likes, the coefficient was converted into an incidence ratio (IRR), which was the unit effect of the dependent variable change on the explanatory variable. The IRR of action disclosure was 2.41, indicating that the number of Likes of digital transformation action disclosure was 2.41 times that of non-digital transformation posts. According to the results, action disclosure was positively and significantly correlated with the number of Shares, while speech disclosure was negatively correlated with the number of shares (significant, p < 0.05), and no significant correlation was found between decision disclosure and the number of Shares. Finally, stakeholders’ reaction was measured by the number of comments generated by each post. Consistent with the results of the first two general reactions, action disclosure was again significantly positively correlated with the dependent variable. However, the results revealed that speech disclosure (p < 0.01) had a significantly negative correlation with decision disclosure (p < 0.05). One possible explanation for this negative relationship was that stakeholders viewed speech or decision making as symbolic, rarely conveying information for the decision, so they were less willing to comment on the disclosure of speech or decision.

Panel B of Table 5 shows the Logit regression results for testing the first set of assumptions when considering specific stakeholder reactions. The research results show the relationship between disclosure strategy and stakeholders’ positive reaction (Love, Great, Wow). The results imply that the three types of hypocritical disclosure (action disclosure, speech disclosure, and decision disclosure) are significantly positively correlated with the reaction of “Love”. However, for “Haha” and “Interesting”, action disclosure is positive, while speech disclosure is negative, and both are statistically significant. In contrast, decision disclosure is not. These results suggest that stakeholders are less impressed with speech disclosure, perhaps because corporate disclosure is consistent with stakeholders’ expectations. Therefore, it is less surprising. The results show that disclosure strategies are associated with negative emotional reactions (Angry) to varying degrees, action disclosure is more likely to lead to anger, while speech disclosure is less likely to lead to anger, indicating that stakeholders are more disappointed with action disclosure. The consistent and positive impact of decision disclosure and action disclosure on anger may indicate that stakeholders interpreted decisions as increasing the likelihood of corresponding actions. Finally, the likelihood of receiving positive comments is only positively correlated with action disclosure, while the similar likelihood of receiving negative comments is positively correlated with action disclosure and negatively correlated with speech disclosure. However, it should note that action disclosure is more correlated with the likelihood of positive comments than negative ones, indicating that although stakeholders have different views on the disclosure of CSR behaviors, on average, they tend not to criticize CSR behaviors of enterprises. In general, stakeholders’ disclosure of CSR actions seems to express opposing sentiments, while their disclosure of CSR conversations is unlikely to receive such conflicting reactions. Combined with the results of general reactions, the correlation between stakeholder reactions and speech, decision, and action disclosure can be known. However, actions, in particular, appear to lead to mixed emotions. Therefore, on the whole, the research results are consistent with previous H1 and H2.

Table 5

Stakeholders’ reactions to CSR hypocrisy disclosure

| Group A Negative binomial regression between general reaction and CSR conversation, decision making and action disclosure | |||||||

| Variable | Likes | Shares | Comments | ||||

| Action disclosure | 0.872***(0.089) | 0.555***(0.076) | 0.461***(0.069) | ||||

| Speech disclosure | –0.058(0.055) | 0.132**(0.056) | –0.256***(0.053) | ||||

| Decision disclosure | –0.003(0.113) | 0.025(0.102) | –0.221**(0.097) | ||||

| Text length | 0.057***(0.016) | 0.208***(0.025) | 0.126***(0.017) | ||||

| Use of photos | 0.379***(0.047) | 0.396***(0.046) | 0.505***(0.041) | ||||

| Use of hyperlink | –0.108**(0.054) | –0.294***(0.054) | –0.260***(0.047) | ||||

| Use of videos | 0.108**(0.049) | 0.076(0.050) | 0.142***(0.047) | ||||

| Enterprise scale | 0.627(0.424) | 0.419(0.478) | 0.300(0.435) | ||||

| Constant | –5.241(4.697) | –3.772(5.298) | –4.563(4.834) | ||||

| Observed value | 362 | 362 | 362 | ||||

| FE of company | YES | YES | YES | ||||

| Monthly FE | YES | YES | YES | ||||

| Pseudo R2 | 0.076 | 0.089 | 0.117 | ||||

| Chi-squared test | 21365 | 13014 | 14639 | ||||

| Investigation>chi2 | 0 | 0 | 0 | ||||

| Group B. Logit regression between specific reaction and CSR conversation, decision making and action disclosure | |||||||

| Variable | Love | Great | Wow | Interesting | Angry | Positive comment | Negative comment |

| Action disclosure | 1.118***(0.078) | 0.711***(0.071) | 0.410***(0.077) | 0.690***(0.088) | 0.614***(0.081) | 0.652***(0.070) | 0.361***(0.072) |

| Speech disclosure | 0.365***(0.053) | –0.243***(0.053) | –0.348***(0.063) | –0.212***(0.077) | –0.133**(0.065) | 0.081(0.050) | 0.276***(0.054) |

| Decision disclosure | 0.277**(0.109) | –0.106(0.109) | –0.190(0.132) | –0.143(0.156) | 0.269**(0.134) | 0.052(0.100) | –0.136(0.114) |

| Text length | –0.075***(0.021) | 0.0495***(0.019) | 0.030(0.020) | 0.027(0.026) | –0.045*(0.021) | 0.064***(0.019) | 0.065***(0.019) |

| Use of photos | 0.460***(0.048) | 0.376***(0.045) | 0.425***(0.053) | 0.157**(0.063) | 0.140**(0.055) | 0.267***(0.044) | 0.200***(0.046) |

| Use of hyperlink | –0.295***(0.050) | –0.137***(0.046) | –0.177***(0.051) | –0.090(0.059) | –0.040(0.054) | –0.189***(0.047) | –0.124**(0.048) |

| Use of videos | 0.198***(0.044) | 0.037(0.043) | 0.139***(0.047) | 0.104*(0.057) | 0.006(0.049) | 0.007(0.042) | 0.010(0.044) |

| Enterprise scale | 0.171(0.437) | 0.919**(0.384) | 1.416***(0.461) | 1.608***(0.532) | 3.100***(0.509) | 0.689*(0.412) | 0.297(0.481) |

| Constant | –4.519(4.884) | –10.216**(5.005) | –19.709***(5.885) | –21.026***(6.776) | –36.158***(6.539) | 6.191(4.602) | –1.568(6.157) |

| Observed value | 20705 | 20620 | 20653 | 20396 | 20730 | 20450 | 20938 |

| FE of company | YES | YES | YES | YES | YES | YES | YES |

| FE of time | YES | YES | YES | YES | YES | YES | YES |

| pseudo-R2 | 0.348 | 0.246 | 0.262 | 0.211 | 0.349 | 0.301 | 0.342 |

| Chi-squared test | 4607 | 5079 | 3815 | 2327 | 4086 | 4609 | 5080 |

| Investigation>chi2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

To test H3(whether stakeholders reflect more on digital transformation action disclosure than on digital transformation speech and decision disclosure), publicity 2 is used. The results in Table 6 show that when an enterprise discloses its actions related to digital transformation, the number of likes, shares, and comments is higher than that of speech or decision disclosure. The results are consistent with H3, indicating that stakeholders reflect more strongly on the action disclosure of the enterprise’s digital transformation than on the speech or decision disclosure of digital transformation, usually showing their approval of what the enterprise has done. However, as the action disclosure of enterprise digital transformation may meet the requirements of some stakeholders but cause damage to the interests of other stakeholders, action disclosure tends to cause more conflicts between stakeholders, which has been confirmed in group B. In group B, the action disclosure of digital transformation is positively correlated with all emotions, and the probability of receiving “Love” is similar to that of receiving “Haha”, and that of receiving “Wow” is higher, suggesting that stakeholders are more impressed when reading about what companies are doing than what they are saying or deciding on the digital transformation of their businesses. In terms of negative emotions, action disclosure of digital transformation is easy to cause sadness or anger and cannot fully meet the different needs of stakeholders, so some stakeholders express disappointment or dissatisfaction. The analysis that stakeholders comment on effects find that although action disclosure of digital transformation is more likely to generate positive and negative comments than dialogue and decision disclosure, the probability of receiving at least one negative comment is higher than that of receiving at least one positive comment. This finding suggests that stakeholders’ negative comments on action disclosure are more likely to occur than in speech or decision disclosure, confirming that it is difficult for speech and decision disclosures to generate negative comments, thus helping to alleviate stakeholders’ concerns.

Table 6

Stakeholders’ reactions to corporate social responsibility disclosure

| Group A. Negative binomial regression between general reaction and action disclosure | |||||||

| Variable | Likes | Shares | Comments | ||||

| Action disclosure | 3.369***(0.136) | 1.255***(0.138) | 3.193***(0.136) | ||||

| Text length | 0.577***(0.129) | 0.438**(0.126) | 0.238(0.130) | ||||

| Use of photos | 0.144(0.074) | 0.469***(0.073) | 0.458***(0.074) | ||||

| Use of hyperlink | –0.288***(0.071) | –0.966***(0.071) | –0.518***(0.072) | ||||

| Use of videos | 0.758***(0.085) | 1.044***(0.084) | 0.663***(0.086) | ||||

| Scale of enterprise | 0.443***(0.034) | 0.975***(0.034) | 0.564***(0.034) | ||||

| Constant | –5.966***(0.711) | –11.196***(0.701) | –6.202***(0.714) | ||||

| Observed value | 362 | 362 | 362 | ||||

| FE of company | YES | YES | YES | ||||

| Monthly FE | YES | YES | YES | ||||

| Pseudo R2 | 0.236 | 0.119 | 0.193 | ||||

| Chi-squared test | 22790 | 14747 | 15060 | ||||

| Investigation>chi2 | 0 | 0 | 0 | ||||

| Panel B. Logit regression between specific reaction and action disclosure | |||||||

| Variable | Love | Great | Wow | Interesting | Angry | Positive comment | Negative comment |

| Action disclosure | 1.385***(0.379) | 1.594***(0.382) | 1.403***(0.381) | 1.324***(0.389) | 1.202***(0.305) | 1.293***(0.381) | 0.986***(0.173) |

| Text length | –0.574**(0.220) | 0.277***(0.081) | 0.506*(0.207) | 0.382*(0.126) | –0.215*(0.089) | 0.351***(0.072) | 0.408***(0.154) |

| Use of photos | 0.502**(0.200) | 0.575***(0.041) | 0.662***(0.255) | 0.327**(0.222) | 0.272**(0.006) | 0.238***(0.351) | 0.214***(0.061) |

| Use of hyperlink | –0.511*(0.201) | –0.383***(0.039) | –0.217***(0.063) | –0.426*(0.206) | –0.231*(0.156) | –0.238***(0.049) | –0.234**(0.045) |

| Use of videos | 0.627**(0.223) | 0.461*(0.219) | 0.278***(0.082) | 0.634**(0.203) | 0.077*(0.036) | 0.123*(0.035) | 0.081*(0.036) |

| Scale of enterprise | 0.179*(0.086) | 0.199*(0.085) | 0.278***(0.082) | 0.383***(0.039) | 0.299***(0.003) | 0.574***(0.041) | 0.041*(0.021) |

| Constant | –5.864(3.240) | –7.917**(2.745) | –17.849***(5.722) | –18.176***(5.789) | –27.139***(6.039) | 7.190*(3.014) | –3.334*(1.028) |

| Observed value | 20705 | 20620 | 20653 | 20396 | 20730 | 20450 | 20938 |

| EF of enterprise scale | YES | YES | YES | YES | YES | YES | YES |

| EF of time | YES | YES | YES | YES | YES | YES | YES |

| pseudo-R2 | 0.446 | 0.288 | 0.329 | 0.331 | 0.351 | 0.410 | 0.367 |

| Chi-squared test | 5220 | 5871 | 3720 | 3189 | 4960 | 4986 | 4720 |

| Investigation>chi2 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

5Discussion and conclusions

5.1Discussion

Information disclosure of an enterprise’s digital transformation on Sina Weibo let stakeholders have the opportunity to understand the relevant information about the enterprise’s digital transformation. However, there are few studies on stakeholders’ reactions to information disclosure of digital transformation. This study verified three types of information disclosure: speech disclosure, decision disclosure, and action disclosure. In this study, a quantitative content analysis method suitable for separating historical materials was used to test the effectiveness of corporate information disclosure strategies in making the public accept information. A total of 632 pieces of information from 19 Fortune 500 companies were analyzed, all of which had disclosure about digital transformation on Sina Weibo. Overall, the posts on digital transformation generate more public engagement though there are differences across industries. The action disclosure strategy is also effective: the data from the negative binomial regression of Table 5 shows that both corporate action disclosure and stakeholder feedback are significant at the significance 0.01 level, which also validates H1a from the data. The public is more involved in posts that contain multimedia formats, such as links, photos, and graphics, as well as interactive messages, requiring the public to take some actions on social media.

The hypothesis focuses on stakeholders’ reactions to corporate behavioral disclosure. Literature shows that factual information can enhance the legitimacy of enterprises [36]. Although the literature acknowledges that action disclosures may help firms maintain stakeholders’ legitimacy (reflected in positive emotions), it also records that they are associated with a higher likelihood of obtaining negative reactions (i.e., negative comments). Related to the previous literature that the legitimacy of enterprises is related to the disclosure of hard information, it is observed that action disclosure is more likely to attract the views of different stakeholders. The empirical analysis is also consistent with the second hypothesis that stakeholders generally respond positively to speech and decision disclosure. The speech and decision disclosure of enterprises’ digital transformation is partially significant and partially insignificant with respect to stakeholder feedback as revealed by the negative binomial regression data in Table 5. Specifically, the speech and decision disclosures of corporate digital transformation are more likely to be “liked”. However, although CSR speech disclosure is less likely to be negatively reflected (negative comments), it is surprising to find that CSR decision disclosure is more likely to cause “angry” reactions, which is possibly because stakeholders may interpret decisions as the likelihood of increasing corresponding actions.

The use of speech and decision disclosures and action disclosure of posts about digital transformation in corporate Sina Weibo shows that enterprises need these three strategies to maintain their legitimacy among different stakeholders and constantly bridge the gap between speech and decision and action to ensure stability, and at the same time, they can also gain more time and flexibility to meet different needs of stakeholders [37]. Since enterprises cannot make progress in all areas simultaneously, stakeholders’ reactions to action disclosure are both positive and negative. However, the negative reaction is mitigated by speech and decision disclosures. Therefore, the results reveal that the stakeholders believe the causal relationship between speech, decision and action, because the speech and decision disclosures of digital transformation are correlated with the high possibility of obtaining “positive attitudes” of stakeholders, and the significant correlation between speech disclosure and negative reaction can explain that such speech disclosure is consistent with social expectations [38]. Therefore, stakeholders are less likely to criticize the wishes of everyone in society if the enterprise’s speeches or decisions on digital transformation conform to social norms. At the same time, these promises of digital transformation are often taken for granted by stakeholders. Therefore, enterprises’ speech is less likely to impress their stakeholders on Sina Weibo, thus leading to a low possibility of receiving positive reactions such as “Wow” and “Haha”. However, once an enterprise discloses decisions, stakeholders will start to have expectations. Studies have shown that the decision to disclose will cause the opposite reaction. However, as Brunsson argues, if there is no hypocrisy, one party or interest will be completely satisfied and the other parties will be completely dissatisfied [39]. If there is hypocrisy, several sides and interests may be somewhat satisfied [because] neither side’s needs are fully satisfied, but neither side is fully satisfied. If stakeholders believe that an enterprise’s decisions increase the likelihood of the corresponding action, those who might benefit from such a decision may express strong support, even if the enterprise does not take any action. Conversely, those concerned with other issues are likely to object vehemently. However, objections only appear in emojis, rather than in stakeholders’ comments, and a greater likelihood of positive rather than negative reactions is observed.

Further, when examining whether there are larger stakeholder reactions to digital transformation action disclosure than speech and decision disclosures (H3), the results from Table 6 show that action disclosure receives more positive and negative reactions from stakeholders than speech and decision disclosures. This is because in terms of the results, the significance coefficients are higher than those in Table 5 in the regressions based on speech and decision disclosure. The data suggest that stakeholders have a higher level of interest in behavioral disclosure.

There are some limitations in this study. First of all, the study assumes that users on social media are stakeholders of enterprises, reflecting their views on information disclosure of enterprises’ digital transformation, but their demands cannot be clearly defined. Secondly, this study only focuses on one social media platform, Sina Weibo. Thirdly, this study cannot distinguish whether the Sina Weibo account of the enterprise is operated by the enterprise itself or outsourced to the public relations agency, and third-party institutions can maintain high participation in enterprises’ Weibo topics with the help of public opinion big data monitoring system.

5.2Conclusions

In this study, the theory of organizational hypocrisy was adopted to investigate stakeholders’ reaction to the legitimacy of corporate digital transformation disclosure on Sina Weibo. By focusing on the dynamic interaction of the subsequent reactions between enterprises and stakeholders at the level of social media and posts, it could be known that stakeholders showed different reactions to the hypocrisy of enterprises, and the intensity and effect of their reactions also affected the reactions of enterprises to the comments of stakeholders after disclosure.

The data from the regression analysis shows that corporate behavioral disclosures are more likely to generate stakeholder interest and positive arguments. The speech and decision disclosures of digital transformation on Sina Weibo don’t allow enterprises to maintain their legitimacy by alleviating negative concerns about the behavioral disclosure of digital transformation. However, when decision and speech disclosure is used as a benchmark, a higher level of stakeholder interest in action disclosure is found.

Empirical evidence combining this conclusion with the previous two sets of hypotheses supports the argument of the organizational hypocrisy theory, which predicts that speech and decision do obtain relevant value, partially satisfy the diverse interests of stakeholders [40], and support previous literature suggesting that action disclosure is more credible. Action disclosure will cause debate among stakeholders, while speech and decision disclosure can gain support from stakeholders and alleviate negative impressions. In general, hypocritical strategies in social media determine how enterprises maintain their legitimacy in stakeholder groups.

In the future, case studies can be used to explore how different stakeholder groups perceive low-criticality strategies and how firms choose strategies based on stakeholder characteristics. At the same time, there can be further extensions for the study population to include the way third-party firms interact with their stakeholders for in-depth analysis.

Acknowledgment

This study was supported by the Academic Research Projects of Beijing Union University (No. SK10202201) and Innovation Centre for Digital Business and Capital Development of Beijing Technology and Business University (SZSK202237).

References

[1] | Lenz-Rashid S. , Supportive housing program for homeless families: Foster care outcomes and best practices, Children and Youth Services Review 79: ((2017) ), 558–563. |

[2] | Kopoin A. , Moran K. and Paré J. , Forecasting regional GDP withfactor models: How useful are national and international data?, Economics Letters 121: ((2013) ), 267–270. |

[3] | Brunsson N. Efectos prácticos de las creencias : El caso de los mercados y las organizaciones (2009). |

[4] | Lyon A. Power struggles involving culture, intellectual cap-ital, and social capital: A knowledge-intensive organization in the midst of change, University of Colorado at Boulder (2003). |

[5] | Christensen M. and Knudsen T. , How Decisions Can Be Organized - and Why It Matters, Journal of Organization Design 2: ((2013) ). |

[6] | Bowen R. and Morris W. , The digital divide: Implications for agribusiness and entrepreneurship. Lessons from Wales, Journal of Rural Studies 72: ((2019) ), 75–84. |

[7] | Laufer D. , Garrett T.C. and Ning B. , The Moderating Role of Power Distance on the Reaction of Consumers to the CEO as a Spokesperson During a Product Harm Crisis: Insights From China and South Korea, Journal of International Management 24: ((2018) ), 215–221. |

[8] | Mcbeath B. , Collins-Camargo C. , Chuang E. , Wells R. , Bunger A.C. and Jolles M.P. , New directions for research on the organizational and institutional context of child welfare agencies: Introduction to the symposium on “The Organizational and Managerial Context of Private Child Welfare Agencies”, Children and Youth Services Review 38: ((2014) ), 83–92. |

[9] | Verschoor C.C. , Consumers consider the importance of corporate social responsibility, Strategic Finance 88: ((2006) ), 20–22. |

[10] | Matt D.T. , Pedrini G. , Bonfanti A. , Orzes G. Industrial digitalization. A systematic literature review and research agenda, European Management Journal (2022). |

[11] | Möller K. and Svahn S. , Role of knowledge in value creation in business nets, Journal of Management Studies 43: ((2010) ). |

[12] | Yang A. and Ji Y.G. , The quest for legitimacy and the communication of strategic cross-sectoral partnership on Facebook: A big data study, Public Relations Review 45: ((2019) ), 101839. |

[13] | Kent M.L. and Li C. , Toward a normative social media theory for public relations, Public Relations Review 46: ((2020) ), 101857. |

[14] | Effron D.A. , O’Connor K. , Leroy H. and Lucas B.J. , From inconsistency to hypocrisy: When does “saying one thing but doing another” invite condemnation?, Research in Organizational Behavior 38: ((2018) ), 61–75. |

[15] | Barden J. , Derry S. , Mcquay H.J. and Moore A. , Bias from industry trial funding? A framework, a suggested approach, and a negative result, Pain 121: ((2006) ), 207–218. |

[16] | Focella E. , Stone J. , Fernandez N.C. , Cooper J. and Hogg M.A. , Vicarious hypocrisy: Bolstering attitudes andtaking action after exposure to a hypocritical ingroup member, Journal of Experimental Social Psychology 62: ((2016) ), 89–102. |

[17] | Neu D. , Warsame H. , Pedwell K. Managing Public Impressions: Environmental Disclosures in Annual Reports, Accounting Organizations & Society (1998). |

[18] | Brunsson N. , Ideas and actions: Justification and hypocrisy as alternatives to control, Accounting, Organizations and Society 18: ((1993) ), 489–506. |

[19] | Lipson M.L. and Mortal S. , The effect of stock splits on clientele: Is tick size relevant? Journal of Corporate Finance 12: ((2006) ), 878–896. |

[20] | Michelon G. , Pilonato S. and Ricceri F. , CSR reporting practices and the quality of disclosure: An empirical analysis, Critical Perspectives on Accounting 33: ((2015) ), 59–78. |

[21] | Barton J. and Mercer M. , To blame or not to blame: Analysts’ reactions to external explanations for poor financial performance, Journal of Accounting and Economics 39: ((2005) ), 509–533. |

[22] | Brown T.J. , Dacin P.A. and Pitt L.F. , Corporate image and reputation in B2B markets: Insights from CI/ARG , Industrial Marketing Management 39: ((2010) ), 709–711. |

[23] | Ahrne G. and Brunsson N. , Organizations and meta-organizations, Scandinavian Journal of Management 21: ((2005) ), 429–449. |

[24] | Cho C.H. , Guidry R.P. , Hageman A.M. and Patten D. , Do actions speak louder than words? An empirical investigation of corporate environmental reputation, Accounting, Organizations and Society 37: ((2012) ), 14–25. |

[25] | Toms J.S. , Firm resources, quality signals and the determinants of corporate environmental reputation: some UKevidence, The British Accounting Review 34: ((2002) ), 257–282. |

[26] | Xu H. , Yang W. and Wang J. , Hierarchical emotion classification and emotion component analysis on chinese micro-blog posts, Expert Systems with Applications 42: ((2015) ), 8745–8752. |

[27] | Koch H. , Yan J.K. , Zhang S. , Milic N. and Curry P. , How Consumer Technology Is Changing the IT Function: A Multi-Case Study of Three Fortune 500 Companies, anagement 36: ((2019) ), 336–349. |

[28] | Smith B.G. and Gallicano T.D. , Terms of engagement: Analyzing public engagement with organizations through social media, Computers in Human Behavior 53: ((2015) ), 82–90. |

[29] | Saxton G.D. , Neely D.G. and Guo C. , Web disclosure and the market for charitable contributions, Journal of Accounting and Public Policy 33: ((2014) ), 127–144. |

[30] | Saxton G.D. , Neely D.G. and Guo C. , Web disclosure and the market for charitable contributions, Journal of Accounting and Public Policy 33: ((2014) ), 127–144. |

[31] | Walsh C.L. , Glendinning S. , Castán-Broto V. , Dewberry E. and Powell M. , Are wildcard events on infrastructure systems opportunitiesfor transformational change? Futures 67: ((2015) ), 1–10. |

[32] | Neu D. , Saxton G. , Rahaman A. and Everett J. , Twitter and social accountability: Reactions to the Panama Papers, Critical Perspectives on Accounting 61: ((2019) ), 38–53. |

[33] | Waters R.D. , Burnett E. , Lamm A. and Lucas J. , Engaging stakeholders through social networking: How nonprofit organizations are using Facebook, Public Relations Review 35: ((2009) ), 102–106. |

[34] | Nartea G.V. , Bai H. and Wu J. , Investor sentiment and the economic policy uncertainty premium, Pacific-Basin Finance Journal 64: ((2020) ), 101438. |

[35] | Saxton G.D. and Waters R.D. , What do Stakeholders Like on Facebook? Examining Public Reactions to Nonprofit Organizations’ Informational, Promotional, and Community-Building Messages, esearch 26: ((2014) ), 280–299. |

[36] | Auger G.A. and Cho M. , Modeling the antecedents and outcomes of perceived relationship investment (PRI) in nonprofit organizations, Public Relations Review 47: ((2021) ), 102083. |

[37] | Christensen H.B. , Hail L. and Leuz C. , Mandatory IFRS reporting and changes in enforcement, Journal of Accounting and Economics 56: ((2013) ), 147–177. |

[38] | Fryer M. Ethics and Organizational Leadership: Developing a Normative Model (2011). |

[39] | Ahrne G. and Brunsson N. , Organizations and meta-organizations, Scandinavian Journal of Management 21: ((2005) ), 429–449. |

[40] | Ahrne G. and Brunsson N. , Organizations and meta-organizations, Scandinavian Journal of Management 21: ((2005) ), 429–449. |